Charter/Broadband Q1 23 Update

Charter/Broadband Q1 23 Update

A look at just how promotional cable wireless lines, and the inconsistency of fiber cost per passing estimates vs actual capex.

Charter (CHTR 0.00%↑ ) was up ~15% post-Q1 earnings (shock!) on the back of ~686k wireless lines and ~67k residential broadband connections, it’s given up most the gains since (less of a shock…). I was a little surprised by the positive reaction as the headline number of 686k wireless connects is a little misleading; broadband performance in their non-rural footprint was the positive from this quarter imo.

Before getting into all that, I want to give a shoutout to Andrew Walker of Rangeley Capital and the author of Yet Another Value Blog. Andrew has one of the bigger blogs in the community but goes out of his way to give the little guy a boost. A lot of you are probably reading this because he linked to my recent Consolidated Communications article in one of his blogs. I’m a big fan of his, so it’s cool to get a shoutout from someone I look up to. If you’re interested in the broadband industry, I’d go read everything Andrew has written on the subject, I’ve read his original Tegus Deep Dive series multiple times.

For those that are new, I usually post a quarterly update (or two) on the broadband industry, with a focus on Charter (which I’m long); I also write-up companies in a variety of industries which I look at as potential investments. I do this for fun but hope, along the way, a few readers find something useful. I am more than happy to answer any questions or comments.

Trending Schedules

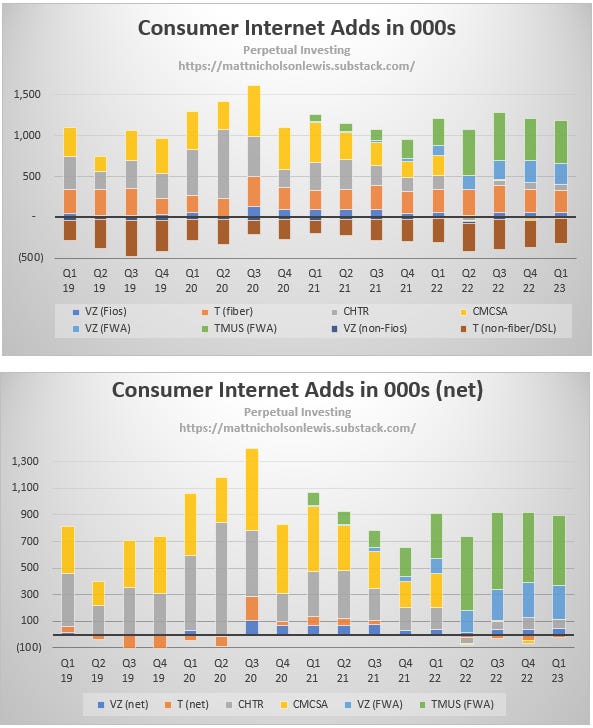

Below are the updated residential broadband trending schedules; T-Mobile’s fwa adds include business connections as they don’t disclose the breakout. This quarter was very similar to Q4, fixed wireless is dominating the market, fiber adds roughly offset DSL losses, and cablecos are starting to show some signs of resilience.

There are a couple of things I’d like to cover in this quarters’ update:

Cablecos – wireless growth and residential resilience

Fiber – Capex spend and management cost per passing inconsistency

I’m going to dedicate a whole post to fixed wireless, as I want to dive a bit deeper on the capacity question (I’ve been meaning to do this for a while). The phrase “capacity limitations” is thrown around as a reason for why fixed wireless can’t compete long-term (me included); I understand why, but defining where that ceiling is is important; is it 20mm connections in rural locations? Is it 30mm with ample capacity in the suburbs? I’m not sure, but it’s something I want to spend some time looking into.

Cable & Wireless

If you haven’t read it already, I’ve written about the cable MVNO strategy in a previous article; it gives some good background on the opportunity and why it shouldn’t be considered a standard MVNO offering.

Charter has pushed their wireless business over the last 6 months with a promotion called SpectrumOne, a broadband/wireless bundle for ~$50 (12-month promo launched in October 2022). Since then, wireless connects have jumped from ~350k a quarter to >600k (they’re now at ~6mm lines with mobile). Analysts, however, have legitimate questions surrounding the quality of these connects, and T-Mobile’s CEO, Mr. Sievert went (way) out of his way to call them “low calorie net adds” in the TMUS 0.00%↑ Q1 cc. Charter’s CEO, Mr. Winfrey, responded saying they are “great adds”, and he expects them to convert to full paying lines post-promo; the truth, believe it or not, is probably somewhere in the middle. A free line is significantly more likely to churn when it becomes a paying line, but Mr. Winfrey is also right, the product is solid and the offer of internet and 2 wireless lines for ~$130 (post-promo) is ~$50 cheaper than what you’ll get from AT&T or Verizon (and similar to T-Mobile’s offer with fixed wireless).

I do think the market is missing how promotional these lines are though, and to use a phrase from Mr. Sievert, if we “double click” on Charter’s mobile adds, it becomes easier to see.

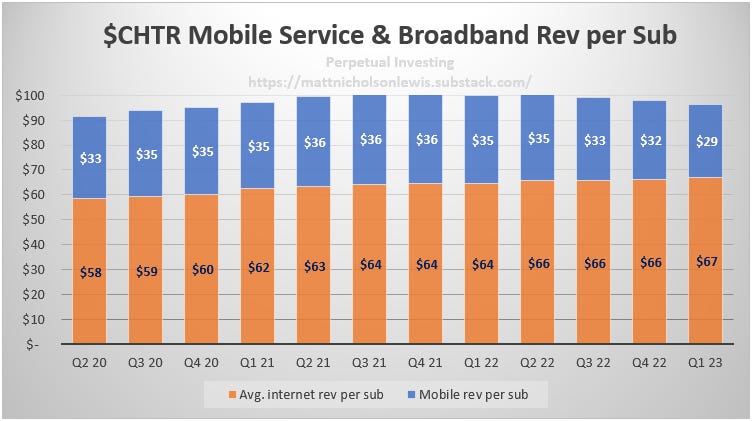

The above chart shows the monthly ARPU for mobile and broadband. Mobile service revenue per subscriber is down ~17% in just two quarters! To put that in perspective, if we assume pre-SpectrumOne promotion ARPU is flat (lines pre-Q3 2022), that means the average ARPU of a wireless sub added over the last two quarters was ~$15. That is what I’d call promotional…

To be clear, I’m a believer in the cable convergence thesis (for CHTR & CMCSA at least), and I agree that the short-term ARPU sacrifice makes sense. It’s a solid product, saves the customer money, uses trusted connectivity branding (Spectrum & Xfinity) to overcome the classic MVNO stigma, and reduces broadband churn. There’s even some potential Ebitda long-term if they can execute on offloading traffic onto their own network (this was negotiated into CHTR and CMCSA’s MVNO agreement and they both own a small amount of CBRS spectrum). To me though, adding 300k mobile lines a quarter at $30, isn’t that different to 600k+ for $15, unless you know they’ll stick as they roll off their promotion (this quarter didn’t give us any new or unique insights on that). I think the market got a little carried away with the line add number.

Broadband Resilience

The residential broadband add number was the big positive for me. Q1 is seasonally one of the better quarters for broadband adds, but there have been suspicions that a lot of Charter’s adds were coming from their rural buildout (RDOF), i.e., losing subscribers in their core market and covering them with high cost rural adds. This quarter management provided new disclosures that showed ~17k of Q1 adds were from the RDOF build, meaning Charter added ~50k residential subs in their legacy footprint. RDOF adds will accelerate as they light-up the network and they’re getting ~40% penetration in 6 months due to low/no competition.

Fiber overbuilders are taking share when they build, but not at a pace that should scare cable (it’s in line with historical builds). The financial situation of some of these pure play overbuilders is also starting to look more questionable. Cable competes on a very local level when it comes to fiber, watching closely as they light up their footprint and then ramping up retention efforts if they see a builder gaining traction. They don’t change advertised price in these efforts, but instead offer more aggressive promos if a customer calls to cancel. This pricing strategy is succinctly described in a Tegus transcript with a former Charter executive (available courtesy of YAVB).

The best competitive situation for a cableco, outside of monopoly or DSL, is a pure play fiber provider that gets itself into financial difficulty and is forced to run for cash. Frontier had this situation during their bankruptcy and lost ~10% share in their Florida, Texas, and California footprint. Larger cablecos who compete across a large portion of an overbuilders’ footprint have an opportunity to create this scenario. CNSL 0.00%↑ competes with Charter and Comcast in ~65% of their footprint, making them a target for this type of strategy (regardless of whether the deal with Searchlight goes through). This is why I prefer larger overbuilders like AT&T or Verizon, as cable has less of an incentive to compete as aggressively. Sure, there’s still competition and cable won’t just give away customers, but there’s solid returns available for both parties in this scenario.

It will be interesting to see if cables’ classic strategy can be adapted to compete vs fixed wireless. Fiber competition is very predictable, it gets announced and then the trucks roll up and start laying fiber; cable knows they’re coming and can track the build very closely. Fixed wireless is different, a cell tower might be upgraded and then, all of a sudden, fixed wireless is available. Cablecos have to predict where the MNO has excess capacity because upgrading a tower or activating a new spectrum band doesn’t necessarily mean they’ll offer home broadband. They also have to know when they’ve used up excess capacity, so they avoid competing against thin air. Solving this problem is key as cable learns to compete with fixed wireless. The good news is it will get progressively easier as the market matures and most of the remaining mid-band spectrum (sweet spot for fixed wireless) lights up over the next year or so.

Fiber and Capex Inconsistency

The fiber overbuild story goes something like this:

“We’re going to overbuild ~70% of our legacy copper with fiber for <$1k a passing and we’ll generate mid-teen IRRs. We’re going to penetrate 15% year 1, 25% year 2, 30% year 3, and get to ~40%+ terminal penetration. The build is fully funded for the next few years and we have flexibility due to a great balance sheet. We’ll start with our most attractive locations and then buildout.”

The likes of Frontier and Consolidated hit their penetration targets for years 1 and 2; I’m of the opinion that getting to 25% penetration is significantly easier than getting from 25-40%. As mentioned above, cable competes on a very local level, getting more aggressive in defending their territory as an overbuilder picks up momentum.

The problem I have with fiber overbuilders is the cost per passing management discloses doesn’t appear consistent with their actual capex spend; the market is becoming more skeptical of this now too. I went through the exercise of reconciling actual capex to management’s comments with Frontier (in my last quarterly update) and my recent Consolidated article and didn’t get particularly close... Frontier then raised their capex guidance for the year during their Q1 cc and got punished by the market, with the stock dropping ~10%, despite adding record fiber subs.

Consolidated didn’t raise their guidance but did do something interesting during the Q1 call; they updated their capex commentary, specifically around how much of their success-based capex relates to consumer vs business or carrier.

“The split of success-based capital is approximately 60% consumers SMB and 40% business and carrier. Please note that consumer success-based capital relates to both fiber and copper installs, includes capital related to our other consumer offerings and includes a modest approximately 10% allocation for indirect costs.”

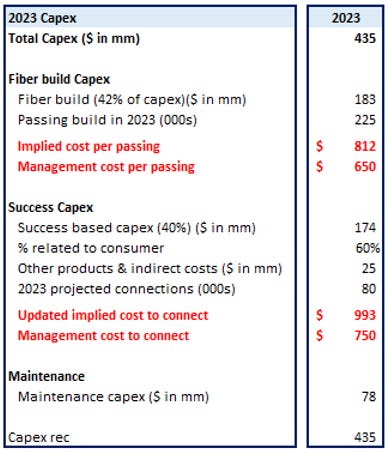

I doubt this had anything to do with my article, but there was some discussion on VIC around it, which Consolidated IR may have picked up on (a fund may have asked management the question as well). I figured it would be good to update the 2023 capex guidance and see if this helps reconcile the questions from my article ($650 cost per passing and ~$800 cost to connect).

Management has disclosed 2023 capex guidance of $435mm (midpoint), of that ~18% is maintenance (~$80mm), 42% relates to the fiber build (~$180mm), with the final 40% success-based, which is capex needed to light up a connection for either consumer/business (~$175mm). Updated management guidance says that 60% of success-based capex is related to consumer and SMB (down from 70%), includes both copper and fiber installs, other consumer offerings, and 10% related to “indirect costs”.

I didn’t include a copper installs component in my article, so I’m going to go ahead and include 10k copper adds and assume they cost the same as a fiber add (copper gross adds are likely ~8-10k a year – using disclosed churn to take a guess at gross adds). For other service offerings and indirect costs, I’m going to assume they’re ~15% of success-based capex (~$25mm). I’d argue indirect costs should be still be included in your cost to build, but it’s not worth splitting hairs over.

These adjustments get us closer, but we’re still over by ~25-30% in relation to their disclosed cost per passing and cost to connect. Maybe I’m missing something else, but at the very least I think you need an answer to this question to be using management’s cost per passing guidance. Then, you have to trust management to hit their capex guidance… It looks like a tougher 18 months ahead for overbuilders.

Final Word

I think overall this was a good quarter, inflation and higher interest rates have hurt highly levered companies like Charter, but the impact to overbuilders is more pronounced due to their negative free cash flow and need for funding over the next few years. I think we see a continued rise in cost per passing for overbuilders and an increased focus on cash generation as the cost of debt stays elevated. This is good news for cable who can fund their DOCSIS 4.0 upgrades from their cash flow for between $100-200 a passing.

Your substack has been a blessing so far. Keep it coming, Matt!