Consolidated Communications: Selling Hopes & Dreams

Consolidated Communications: Selling Hopes & Dreams

A look at Consolidated Communications fiber buildout. Management has issued a lot of positive guidance but has consistently come up short.

Summary

Consolidated Communications is a story we’ve heard before; a legacy telco upgrading their obsolete copper footprint to fiber. They currently pass ~2.6mm homes and have built fiber to ~1mm of those passings (they plan to get to ~2mm). Analysts expect Consolidated to generate ~$1.1bln in revenue and ~$310mm of Ebitda in 2023. The business currently trades at ~7.5x NTM EV/Ebitda.

If you are bullish on fiber and believe overbuilders rapidly get to their terminal penetration targets (~40%+), you might think Consolidated (CNSL 0.00%↑) is a good stock to own; It’s highly levered and aggressively building out fiber to >70% of their footprint. I have a different view, Frontier (FYBR 0.00%↑) is a better way to make that bet imo (I’m not long either business). Some key reasons why I prefer Frontier:

Frontier has a significantly better balance sheet

Frontier management has proven they understand their business and have hit on key fiber metrics

They slowed their fiber build by ~20%, vs >40% for CNSL

Frontier’s is further along in their build, it’s a bigger part of their business, and they trade at a cheaper multiple (~6x vs ~7.5x EV/Ebitda)

Private equity involvement and a new brand adds risk to CNSL

Let’s get into the details.

The Situation

The current Consolidated story starts in 2020. After a series of underperforming acquisitions, they were left with an obsolete copper footprint and a mountain of debt. Management was using all available cash flow to paydown debt in the hopes of avoiding bankruptcy.

Things changed in late 2020, when Searchlight, a private equity firm, provided ~$425mm in financing and effectively saved the business; the transaction was structured in 2 stages, with $350mm received upfront and another $75mm after FCC approval. In return, Searchlight received a $395mm preferred (9% coupon) and ~35% of the company (note: there were some additional steps to get to the 35%, but that is where we are today – FCC approval was granted late 2021). As part of the deal, Consolidated obtained the option to let preferred interest accrue and increase the principal; they plan to use this option through at least 2025. The preferred principal is currently ~$475mm (as of 12/31/2022). They also refinanced debt and extended maturities until ~2028.

In conjunction with Searchlight’s investment, management laid out plans for a significant investment in fiber.

The upgrades were focused on Consolidated’s Northern New England footprint (previously FairPoint), where management believed they had a significant advantage due to its fiber deep network, and ~80% of the plant being aerial. They planned to upgrade ~1mm passings in the region for ~$450mm ($450 per passing).

In total this meant ~$2bln capex spend (this is all-in capex), from 2021-2028 and ~1.6mm new fiber passings, ending up with ~2mm total (they slightly increased the passing total post original announcement).

Consolidated footprint as of June 2022 – red=copper footprint, green=fiber, blue=cable

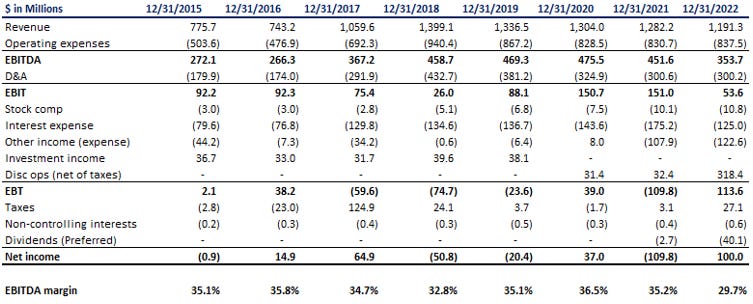

Fast forward to the end of 2022 and Consolidated passes ~1mm locations with fiber (~725k built in last 2 years) and has ~125k fiber connections. They’ve monetized ~$625mm of non-core assets to fund the buildout (~$500mm from wireless partnerships and ~$125mm from their Kansas and Ohio operations), and launched a new fiber brand called Fidium. Historical financials below.

The Issues

This is a classic fiber overbuild story on the surface, turn ~10% copper penetration into 40%+ with fiber and increase ARPU by ~25%. I have concerns about Consolidated, some are shared by other fiber builders but a lot are unique to CNSL:

They have significant leverage and little to no margin for error

They have consistently missed projections

This is a fiber story, but fiber only makes up a small portion of their business (and will for a long time)

Even if the business turns, private equity involvement and cables’ competitive reaction adds risk

Let’s go through them.

Leverage

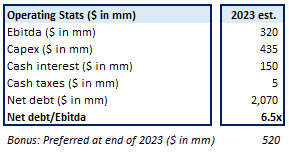

Put simply, CNSL’s fiber strategy needs to work fast; some 2023 numbers:

Using the midpoint of the most recent guidance provided by management, Consolidated will end 2023 with a net leverage ratio of ~6.5x unless additional financing is secured; this is getting close to tripping some of their debt covenants. The preferred will be ~$520mm due to another year of accruing interest at 9% (not included in net debt/Ebitda); the preferred is obviously relevant if you’re thinking of investing in the common.

Management is guiding to mid-teen Ebitda growth in 2024, but even if Ebitda inflects, there’s at least $550mm of capex and cash interest over the next few years; this means we’re looking at ~$150-200mm cash burn, annually. The 2028 debt is currently yielding ~14%, refinancing or issuing new debt will be expensive.

Management

Management came out with some eye-popping projections when they announced their buildout, with $450 a passing being the headline grabber. Unfortunately, they’ve missed a lot of them over the past couple of years. Reading through old transcripts this becomes all too obvious…

$450 a passing – Northern NE footprint

Analysts were skeptical of the $450 cost per passing right out the gate; quote from the Searchlight investment announcement:

“Can I just have a follow-up on the $450 per home passed for fiber? How is that possible?”

Management pointed to deep fiber and aerial plant, even claiming $450 per passing was “conservatively high”. They’ve since backed off the $450 number, but still claim their overall cost per passing is ~$650 (this includes the non-Northern NE footprint), with a cost to connect of ~$750-800.

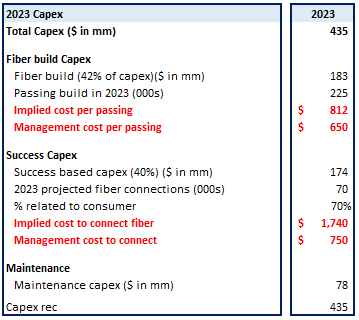

In Q4 management gave some additional details on 2023 capex spend, disclosing ~42% is supporting the fiber build, ~40% is success based (cost to connect etc.) and ~18% relates to maintenance. They also disclosed that ~70% of their success based capex relates to consumer, with the other 30% carrier and commercial. We’re going to get into some numbers here, but I think it’s important to show the math.

I’m sure there’s other capex items that could help explain some of the smaller differences, but directionally what this shows is management is extremely optimistic. The biggest difference comes on their cost to connect, where the ~$750-800 is nowhere near what I calculate. Sure, I could be wrong on fiber adds (I’ve projected ~75% growth) and there’s probably some other activity, but I don’t think I’m off by >100%! It’s also worth noting their capex guidance has been consistently off since announcing their build, with 2021 guidance ~$410mm (actual ~$515mm) and 2022 ~$485mm (actual ~$600mm).

They guided to ~$2bln total capex spend when they announced the plan in 2020. They’ve spend >$1bln in 2021 and 2022, and are ~40% through the build… Some more examples of management guidance below.

They claimed fiber build was “fully funded”.

They claimed Ebitda would grow sequentially at the at the end of 2022 and full Ebitda growth in 2023 (they’ve pushed this back to 2024 after Ebitda dropped ~$100mm in 2022). To be fair ~$50mm of the Ebitda decline was due to monetizing ~$600mm of assets, but even normalizing for this they were way off.

Disclosed a buildout target of ~400k passings in 2023, but at the end of 2022 they dropped this by ~45% to ~225k. To add some context, they beat their build projections over the first two years (by ~30k), and they said a “minimum” of 225k passings, but a reduction of this magnitude is likely linked to lower-than-expected penetration and higher-than-expected costs (conserving cash?).

Morgan Stanley Conference 1/6/2021

“I think our target leverage is to be below 3x by 2025, if not sooner”

I’m not expecting management to be perfect, but they have consistently been overly optimistic with their fiber build guidance. To be frank, I think it’s difficult to take management at their word at this point (calling them optimistic is the charitable take).

Fiber story

The market rightly focuses on the fiber transformation for Consolidated (and other legacy telcos), it’s a futureproof technology with a significant runway for growth, but this focus can make investors overlook other significant headwinds; this is especially important given CNSL’s leverage.

In 2022, CNSL made >$300mm of revenue from legacy voice services, ~$75mm of video revenue (assuming ~$25mm from commercial), with the remaining made up from either data services or network access. When giving the 2023 Ebitda bridge, management called out a headwind of ~$20mm related to legacy voice; this is a huge number on ~$310mm of Ebitda.

Only ~$80mm of revenue was from residential fiber. This is growing quickly (Q4 grew 50% YoY), but even in a bull case scenario (500k connections and $75 ARPU in 2027), they’ll still only generate ~$450mm of fiber revenue (<40% of 2022 total revenue). To be clear, if Consolidated is generating $450mm of fiber consumer revenue in 2027, this investment works in a big way (assuming they can finance the build), the point is the business is made up of a significant amount of legacy technology (copper, voice, and video); it’s not just replacing copper broadband for higher ARPU fiber.

What if it works?

Cable response

The biggest problem I have with the bull thesis for fiber is the 40%+ terminal penetration in ~5 years assumption. Hitting the early penetration targets is significantly easier than grinding from ~25-40%. A Tegus call with a former Charter executive gives some insight into how cablecos deal with a fiber overbuilder:

“The first thing we're going to do is nothing. We're going to watch them like a hawk… How many new customers are you winning each month… or churn, are we starting to lose more customers?”

If we're not seeing a material change in that, we're not going to do anything even though there's more fiber there because they've just proven they're not good enough to go to steal our customers, so we're not going to go pay the market because we're afraid of something that we have no means to fear. Now if after a couple of months… they're actually stealing share either because the trajectory of connects has changed or our churn profile has changed…, then we're going to do something.

Basically, cables’ reaction depends on an overbuilders’ success. ~70% of Consolidated’s footprint (and pretty much all of the Northern NE footprint), overlaps Charter or Comcast. There are also some hints that CNSL’s fiber adds are not necessarily mass-market consumers, with >70% of new signups choosing their 1-gig service. This is great for ARPU (CNSL has 1-year deal at $70 before jumping to $95), but to me, this points towards broadband nerd type sign ups; the average household just doesn’t need a 1-gig symmetrical connection.

To get to 40% penetration you need a significant number of “normal” customers, most of which are just looking for the best deal and a product that works. The usual defense for cable, when a customer attempts to leave, is to offer a reduced price for the next 12-months or some kind of sweetener; the more concerned they are the more aggressive they get.

Consolidated is in a bad position here, they need quick penetration due to their leverage and they compete against the two largest cable providers in ~70% of their footprint. If I’m Comcast or Charter, this is the kind of overbuilder I want, financially fragile with a new brand and an unproven management team; I would get aggressive on promotions to customers that are thinking of leaving and just wait for CNSL’s leverage to force them to run for cash, then let off the gas.

This is why I think overbuilders like AT&T and Verizon do better, their strong cash flow provides a significant cushion if cable decides to compete aggressively. In this scenario, cable likely accepts a duopoly and focuses on returns.

Private equity

Let’s say you believe my analysis is way off (believe or not it’s possible...) and you’re bullish on fiber and Consolidated; you now need to get comfortable with a significant minority shareholder who owns ~35% of the company, has 2 board seats, and a $500mm preferred ahead of you in capital structure (the 35% common stake is only worth ~$100mm). Full disclosure, I haven’t looked too deeply into specifics of how they could do this (I never got comfortable with bull thesis in the first place), but given the risk involved here, you need to be sure you’ll get the upside if this works. Searchlight filed a 13D back in early 2022 but hasn’t increased their stake, despite CNSL stock being down >60% since the beginning of last year.

Valuation

Consolidated trades at ~7.5x NTM EV/Ebitda, compared to Frontier which is ~6x. I struggle to justify, through a relative value lens, why Consolidated is the better choice here. Frontier’s management has proven they can hit their fiber buildout targets and that they understand the business, they’ve shown sequential Ebitda growth (end of 2022), they don’t have the minority shareholder risk, they’re better financially positioned, and they haven’t slowed their buildout as much.

Consolidated does have more “moonshot” potential due to their leverage and starting point (they only had ~250k fiber passings pre-fiber strategy announcement), but I think you’re taking a massive amount of risk and attaching yourself to a management team that has given you no reason to trust them (as well as the PE risk).

Final word

There’s a detailed write-up on VIC if you’re looking for a bull case to compare this against, but I’ll be staying away from CNSL. I think duopoly fiber vs cable is the inevitable end point, but if I’m a cableco and I’m going to get overbuilt, I would love it to be CNSL. Charter and Comcast can tailor their response to keep CNSL under financial pressure, knowing CNSL has limited time to hit their penetration targets before they have to run for cash (this is likely why they lowered their build target in 2023).

Searchlight buyout offer at $4 a share (~$460mm implied market cap or ~$2.6bln EV). Obviously good news for the stock short-term but will be interesting to see what CNSL investors think; stock started the year ~$4, so this likely locks in a loss for most. I suspect most were looking at CNSL as a high risk bet with massive upside potential, so locking in at $4 isn't that exciting to them.

Offer makes sense for Searchlight but definitely aggressive - get control of business for $300mm more and direct how they recoup their investment (>$500mm with preferred accruing). Also mentioned they would invest more capital to fund the fiber build, hinting the build isn't currently fully funded..

https://www.sec.gov/Archives/edgar/data/1304421/000119312523099940/0001193125-23-099940-index.htm

Interesting that Eric Zinterhofer of Searchlight bought Charter's stock from market roughly at end of last year (thinking emoji).