The Wireless Opportunity for Cable

The Wireless Opportunity for Cable

A deeper look at cablecos' wireless offering and it's long-term outlook.

Cable stocks have been beaten down over the last year due to aggressive fiber overbuilds and the emergence of fixed wireless. Broadband adds have slowed, and the market is now questioning where the next leg of growth comes from (if any). This article will focus on cable’s wireless offering and how it can help in their fight against new competition.

Note: cable/cableco refers to Comcast/Charter.

Wireless has been a bright spot for cable, with $CHTR and $CMCSA adding ~10mm lines since their launches in 2017/18. Despite this, investors are struggling to put a value on the revenue stream. There are two key reasons why:

They’re approaching scale and not making much of a profit. Both Managements say they expect long-run margins to be reasonable, but wireless currently loses money for Charter and roughly breaks even for Comcast.

They don’t own the infrastructure. They run using an MVNO strategy (Mobile Virtual Network Operator) on Verizon’s network, so owners’ economics are unattainable (low margin product).

Despite this, I think the market is underestimating Comcast/Charter’s wireless business, and I’ll layout why in this article. To be clear though, wireless will not “save” cable, it is a complimentary offering that can help against new competition and reduce broadband churn.

But first, a little history will help understand the opportunity.

History

Cables previous flirtation with wireless ended in 2011, when Comcast and Charter (then Time Warner Cable and Bright House), operating under a JV called SpectrumCo, essentially gave up on building their own wireless network. They had purchased 122 AWS licenses in 2005 (for ~$2.5bln), but never found a way to utilize the spectrum; instead, they agreed to sell them to Verizon for ~$3.6bln.

The agreement also included areas where Verizon and SpectrumCo would collaborate. They both agreed they could sell each other’s services in their own stores (cross selling agreement – Verizon could sell Xfinity broadband/Comcast could Verizon wireless), and SpectrumCo obtained the right to resell Verizon’s wireless services under their own brand.

The deal came under regulatory scrutiny and, to get the deal approved, Verizon made additional concessions. First, they agreed they would not cross sell their services in areas where they competed with SpectrumCo (where Verizon offered Fios), agreed to a 5-year time limit on cross-selling before getting reapproval from the DOJ, and agreed to sell some of their spectrum to T-Mobile.

The key for cablecos was Verizon’s legal requirement to provide them wireless services. Below is the quote from the final judgment:

Details of the amended agreements have never been made public, and the last sentence isn’t relevant as both have now launched their products, but the right to use Verizon as wireless provider has proven very useful.

The Opportunity

So, why does this opportunity even exist? MNOs like Verizon, AT&T and T-Mobile typically use MVNOs to access certain market niches outside their core customer base. In a perfect world MNOs generate incremental revenue by renting out the additional capacity on their network, all from customers they couldn’t reach anyway (no cannibalization).

A full service MVNO runs on the MNO’s network but bills and manages the customer relationship separately, under their own brand; this is how Comcast and Charter operate. Unfortunately for MVNOs, margins are typically very low (Ebitda margins avg. ~10%), with the MNO reaping most of the benefits. However, cablecos have several small advantages over a classic MVNO that make their offering more valuable:

The legal agreement with Verizon changes the dynamics when it comes to negotiating contracts. MVNOs are typically at the mercy of the MNO when having to renegotiate deals, but cablecos have a starting point for negotiations that tip the scales in their favor.

Cablecos are selling a bundled product, so the goal of their wireless offering is more than just profits. If offering wireless reduces customer churn, it increases lifetime customer value.

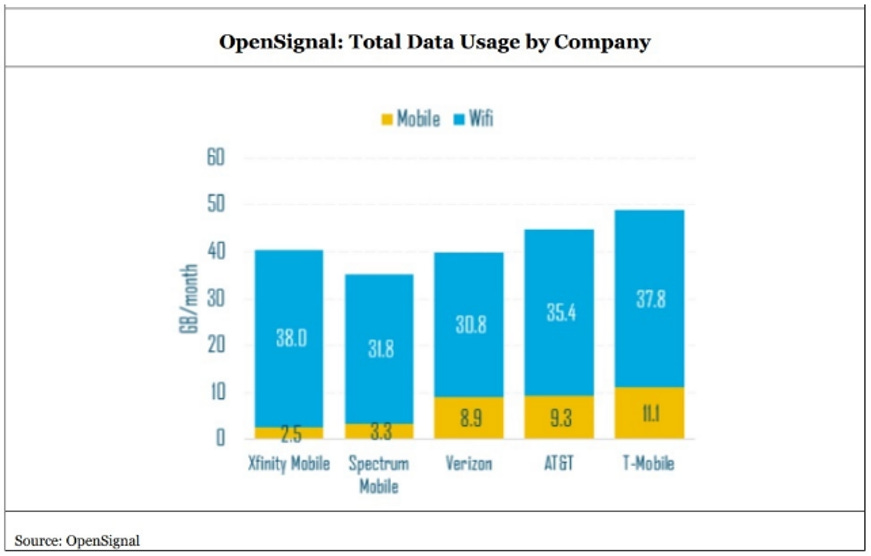

Cablecos offload up to 90% of network traffic to home WiFi or hotspots. They also own CBRS spectrum they can potentially use to offload traffic onto their own network. Keeping traffic off Verizon’s network reduces the payments they have to make to Verizon and increases their potential margins.

Let’s look at these in more detail.

Reseller Agreement

As mentioned above, the details behind the reseller agreements with Verizon aren’t public, but we can still get a sense of the agreement from public filings and management comments. First, and most important, cablecos use the word “perpetual” when describing their agreements. Comment from Brian Roberts, Comcast CEO, at Goldman Sachs 2020 Communicopia Conference:

This is significant as it means Verizon can’t pull the service if cablecos start having too much success. It also helps negotiate with other MNO’s and leverage a better overall deal. They did just this to negotiate a new deal in November 2020.

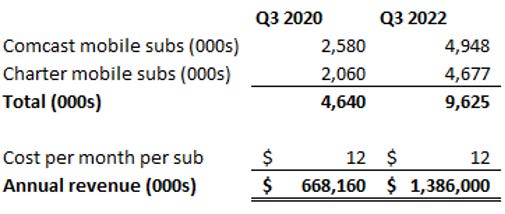

The agreement was signed ~3 months after Tracfone penned a new MVNO agreement that increased their Ebitda margins from ~9% to 15%. Additionally, at the time of the renegotiation, there were rumors that AT&T was looking at potential wireless deals with cable companies. It’s been reported Verizon makes ~$12 a subscriber (per month under the new agreement) from cablecos, so at the time of the deal that would be ~$650mm in annual revenue for Verizon (~$1.4bln now).

This is not inconsequential revenue for Verizon, and with cablecos able to fall back on their legal agreement, both Verizon and AT&T are incentivized to push for the business, even if the deal might undercut their own wireless operations (cablecos can’t be pushed out the market).

Piecing this together, the evidence points to cablecos being in a good negotiating position at the time of the deal; however, assuming a Tracfone type deal is probably too simplistic (Tracfone deal was signed ~3 months before Verizon acquired them).

It was reported as early as 2015 that the original SpectrumCo/Verizon agreement was “stale”. The limitations were mainly around plan flexibility and data pricing. This likely gave some leverage back to Verizon, with cablecos willing to give up some of the economics for more flexibility on plans and pricing.

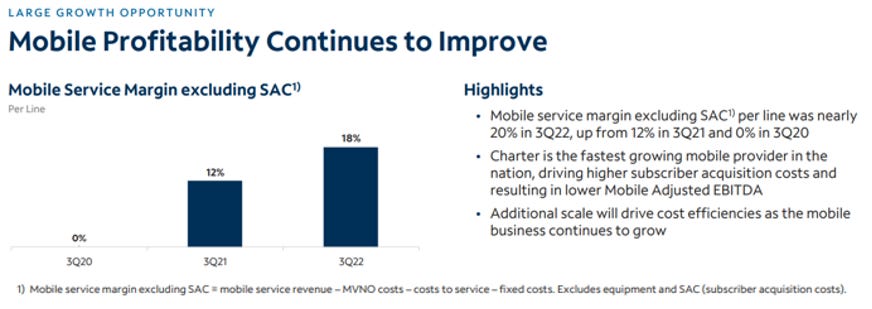

Charter also gave some detail at their recent investor day, disclosing service margins have increased from ~0%, before the renegotiated deal, to ~18% as of Q3 2022 (overall mobile Ebitda is still negative). A lot of this increase can be attributed to scale efficiencies, with subscribers increasing from ~2mm in Q3 2020 to ~4.7mm as of Q3 2022, but it’s likely some relates to an improved agreement.

I think normalized Ebitda margins end up in the 10-15% range, but we’re a long way from seeing those type of margins as cablecos continue to chase growth. We might never truly find out, as both Charter and Comcast are stopping wireless Ebitda reporting. While I’d prefer they keep reporting this figure, they don’t report video or broadband margins, so this was inevitably going to disappear under their “convergence” strategy.

Bundled product

This concept isn’t new to those of us who have followed the cable industry for a while. Bundling products helps increase the value of each subscriber by increasing revenue per sub and reducing churn. Cable’s classic triple play of broadband, video, and voice is dying, right at the time competition is increasing. I think there’s an argument the legacy bundle actually hurts cable now, with video fees way out of line with value.

Wireless is a way for cablecos to replace video with a product that offers real value to their customers. There are a few reasons to think this is possible:

It’s been done elsewhere. In Europe, it’s estimated that ~37% of broadband households are bundling wireline and wireless products. It’s currently just 8% in the U.S.

Customers are open to switching wireless providers. A 2018 study from Barclays found that ~40% of respondents would consider switching to a wireless offering from their cable provider. Of those that weren’t open to switching, nearly half said they would reconsider if pricing was lower.

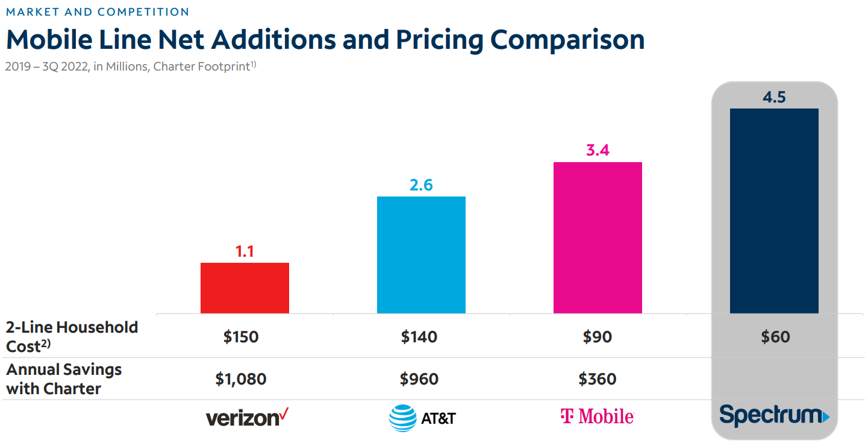

If cable can offer a cheap product that reduces customers’ bills, there’s no reason cablecos can’t keep growing wireless subs for the foreseeable future. They’re currently ~5% household penetration and while people like to hate on cable for their promotion and price hike strategy, it works. In Charter’s case, under SpectrumOne, they’re offering a bundle that costs ~$120 on a standalone basis (broadband and 1 wireless line), for ~$50. This should help incentive customers on the fence, even if it pressures ARPU short-term. Tougher economic conditions may also open customer minds to a cableco wireless product.

Data offload

Running a wireless network is incredibly expensive, you’ve got the massive infrastructure buildout (towers, radios etc.), as well as the spectrum which can run into the 10s of billions of dollars. It’s easy to understand why cablecos gave up and pushed for the reseller agreement instead. It’s also easy to see why MVNO’s earn low margins. You’re at the mercy of your MNO, and while you can negotiate with all three (AT&T, Verizon, T-Mobile) for the best deal, the reality is you need them more than they need you.

This is where the new agreement comes in. Cablecos negotiated the right to offload traffic onto their own wireless network. Only ~10-15% of traffic travels over Verizon’s network currently, and while this 10-15% is essential, lowering this percentage by a small amount could have a big impact on the economics for cablecos.

Comcast/Charter spent ~$900mm on CBRS spectrum in 2020 and are trialing offloading traffic onto their own network. They claim they don’t need to do this for wireless to be profitable but are looking to offload data in dense areas. They’ll always be reliant on an MNO, but the more data they can get off the network, the more economics they can extract from the business.

It’s also one of the largest risks. The quality of cablecos’ offering has been well received, mainly as they’re running on Verizon’s network. But rolling out a wireless network opens them up to execution risk, and seamlessly transitioning between two networks adds complexity, requiring dual-SIM technology.

Risks

Speaking of risks, what are the key risks that could trip up cable’s wireless offering?

Customers despise their cable provider more than I understand, and not for just video pricing; also broadband at ~$70 a month. If this group is large enough, it will severely impact the potential number of people willing to consider cable wireless.

Execution risk related CBRS spectrum. Cablecos will be on a short leash with their wireless offering (customers expect their phones to work). If they stumble in rolling out their mini-network, they’ll lose customers. Management has executed on the wireless strategy so far, and they’ve earnt the right to be trusted here, but operating your own wireless network is a big leap from managing back-end functions.

MVNO deal risk and ceiling on growth. While most signs point in the direction of a good deal for cablecos, there’s a limit to how large the wireless business can get; it all comes back to, you guessed it, not owning the infrastructure. Verizon will get more and more creative if cablecos start significantly encroaching on their core customer base (agreements can be broken). Inherently, operating as MVNO means you’ll be a smaller player in the space.

It doesn’t reduce churn. Wireless is not going to be a big earner (10-15% margins). The value comes from reducing customer churn. I don’t see how it doesn’t; it makes changing broadband provider significantly more involved. You have to sign-up to 2 new services when you cancel, and the new broadband provider might not bundle wireless and broadband. But if, for some reason, wireless doesn’t reduce churn, you have, at best, an earnings replacement for video and no help fighting new competition.

Summary

There you have it, why I think the wireless opportunity is a valuable product for cable (and where I could be wrong). While I don’t think penetration reaches 50%+ like broadband, I could see wireless getting to >20% household penetration at maturity, with an average of 2 lines a household. Using Charter as an example and ~$50 as ARPU, that’s ~$13bln in revenue and $1.3bln of Ebitda (10% margin) at maturity. This would just about replace video and would be ~5% of Charter’s current consolidated Ebitda.

The key again is how much it impacts churn. A significant number of opportunities for broadband connections (and disconnects) come from mover churn. You move house or apartment, and the customer acquisition process resets (you’ve got to reacquire the customer all over again). But in 2021, ~50% of moves were cross-town and ~80% were intra-state. Meaning, most movers likely stayed within their cable providers footprint. This situation is perfect for the wireless bundle; you remove the need to reacquire the customer as the wireless relationship doesn’t require a direct wire into your house.

Thanks for reading.

Great write up but I think your mobile margins are way off. https://www.bamsec.com/transcripts/f7292268-b08b-4fed-b336-c7ed39e8c675

Nice work.