Cruise Lines: Not too Late to Jump Onboard

Cruise Lines: Not too Late to Jump Onboard

I own RCL & CCL on a sector bet. I think cruise lines grow earnings and reduce leverage as they take advantage of reduced new capacity over the next few years.

Cruise lines have had a tough few of years. The pandemic famously put a halt to sailings for >500 days and forced operators to issue both debt and equity to survive. They’ve come out the other side with diluted shareholders and significant leverage; I think their future is bright now though, and the industry is setup for significant earnings growth due to robust demand, moderate capacity growth, and a capital allocation strategy focused on debt reduction.

I own both Carnival and Royal Caribbean on a sector bet — CCL 0.00%↑ has the most upside given their leverage profile, and RCL 0.00%↑ is the best-in-class operator trading at a higher multiple (RCL is also already operating at pre-pandemic margins). This post will focus on the overall industry. I’ll do a follow up on the individual companies.

Industry Background

The industry is reasonably simple to understand. Cruise lines spend a significant amount of capital building ships (capital intensive business); a ship can cost up to $2bn for a megaship like Royal Caribbean’s Icon of the Seas (~5,600 passengers not including crew). The process of designing, building, and getting a ship ready for commercial use can take >5 years depending on its size and specifications. There are only 4 shipyards that can build cruise ships, and all are located in Europe.

Cruise lines own their ships (they don’t lease) due to favorable financing terms with Export Credit Agencies (ECA) — rates are usually ~3-5% and amortize over 12 years.

There are a lot of different types of cruises, but they can very roughly be grouped into three categories:

Contemporary — large/mega ships that include brands like Royal Caribbean, Carnival, and Norwegian (~2,500-6,000 capacity). Ticket costs hypothetically cover an all-inclusive experience, but things like Wi-Fi, soda, alcohol, and specialty dining usually cost extra. Average ticket cost is ~$50-450 per person, per day.

Premium — More refined and more spacious experience, with capacity usually <3,500. Celebrity and Princess are examples of premium cruise brands. Average ticket cost is ~$300-700 per person, per day.

Luxury — Smaller ships and have very high staff to customer ratio. Usually only a few hundred guests, with an avg. nightly rate of >$600 per person (can run a lot higher). Luxury cruises are more likely to be truly all inclusive, with activities like day excursions and butler service included.

Customers purchase tickets ~6-12 months before a cruise sets sail. This allows operators to fund the business with customer deposits (liability on the balance sheet) and operate with a negative working capital position. This created a major issue when sailings were cancelled during the pandemic (needed to reimburse billions to customers). ~65% of cruise revenue is generated from ticket sales, with the rest coming from onboard activities like day excursions, specialty dining, and Wi-Fi.

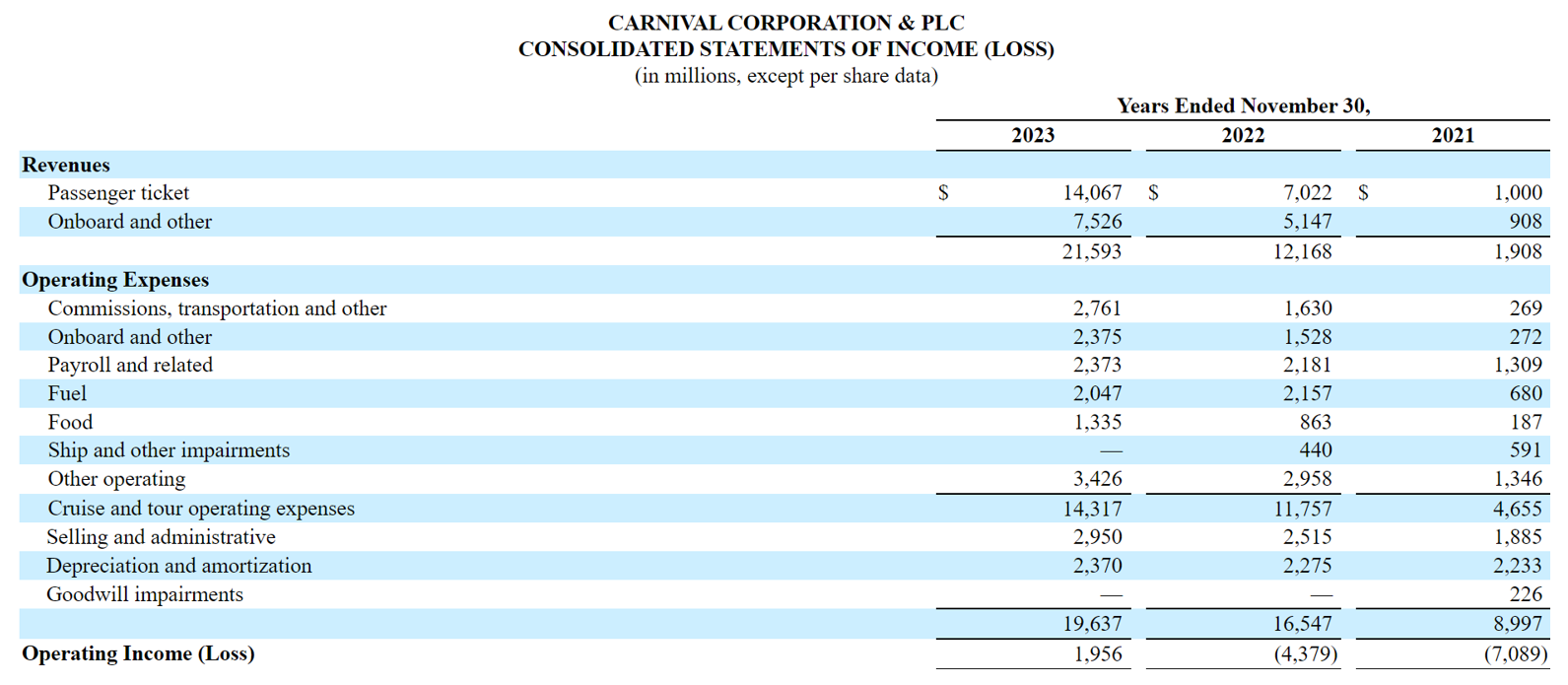

Cruising is a fixed cost business (incremental cost for an additional passenger is very low). Because of this, if a sailing is undersold, operators offer heavily discounted tickets to fill up ships; this has been less common post-pandemic due to strong demand. Key costs include commissions, transport (e.g., flights to port), payroll, food, and fuel (some operators hedge fuel costs); cruise lines also get the benefit of not having material tax liabilities due to Section 883 of the IRS code (this could change from 2026 with a new minimum tax). Detail of costs can be seen in Carnival’s 10-K below:

There are ~360 cruise ships in operation across the globe with a passenger capacity of ~700,000 (avg. ship capacity of ~2,000). Four cruise lines — Carnival, Royal Caribbean, MSC Cruises, and Norwegian — make up >80% of the industry’s capacity (operating across multiple brands).

Cruises have grown in popularity over the last couple of decades, growing from ~12mn passengers in 2003, to ~30mn passengers in 2019. There are a few reasons for this growth; first, demand has increased as they offer a cheaper vacation alternative. Morgan Stanley estimates a cruise is ~25% cheaper than a land-based vacation, up from ~35% in 2022.

Second, the quality of the offering has increased as new tech has allowed for cruise lines to build “floating cities”, rather than just large ships; the increased size creates more room for activities (waterparks, adult only areas etc.), restaurants, and better unit economics per berth. The large size does create logistical headaches for docking and can reduce itinerary flexibility (some islands don’t even have the infrastructure to facilitate a megaship docking), but overall they create better economics for cruise lines.

Modern cruise ship vs Titanic

Next, they reduce the complexity of a vacation; families can book a cruise and effectively outsource the planning of their vacation to an operator like Royal Caribbean or Carnival. Additional activities such as land excursions or evening shows are on offer (sometimes for an additional charge), but a family can relax knowing there will be something for everyone to do. Cruises can also dock at their own private islands to offer a curated land-based option for guests (e.g., Royal Caribbean’s CocoCay).

Cruises have a very small portion of the travel and tourism market. The below pie chart from Carnival is a bit misleading (chart crime), the cruise industry’s TAM is nowhere near the full $5.4t of travel and tourism spend, but it does show cruises make up a tiny part of the market; a very small share gain would lead to significant industry growth.

Cruises are admittedly a niche and surprisingly divisive vacation option (it’s a love or hate product), but there’s a long growth runway for demand growth — only ~7% of Americans have ever been on a cruise.

Why is the Industry Appealing

I think Cruise lines are appealing for a few reasons. They have a solid growth runway, limited new capacity over the next few years, certainty over capital allocation, and trade at close to long-term average multiples while still regaining pre-pandemic efficiency.

Some of my recent investments over the last year have followed a similar playbook — MPC 0.00%↑ has nearly doubled since I purchased (Q2 23) on resilient demand, limited capacity, and consistent buybacks (can read the post here). My airline thesis is along the same lines, I’m roughly flat on AAL 0.00%↑ since Q4 23, with limited new capacity due to supply chain issues, destruction of the ULCC model (Spirit/Jet Blue decision has helped here) and a focus on paying down debt.

Cruises offer a similar setup in that capacity growth will be moderate over the next few years and debt reduction is the focus; where cruises lines get really interesting is the outlook for top line growth.

Growth

As mentioned above, the cruise industry has consistently grown over the last couple of decades, from ~12mn passengers in 2003, to ~30mn in 2019.

The industry, ironically given the shutdown of operations during the pandemic, has shown an ability to grow through multiple different macro cycles and events, including 9/11 and the 2008 GFC. Outside of another viral event like covid, continued growth in passengers feels like a good bet. The Cruise Line International Association (CLIA) agrees, predicting ~38mn cruise passengers in 2026 (~30% increase from 2019).

Cruises are popular among all age groups but skew older (avg. age ~48), especially baby boomers who continue to retire with significant wealth; ~33% of passengers are baby boomers and the vast majority plan to cruise again. The percentage of the population open to cruises also appears to be growing. In Q3, RCL disclosed that ~67% of their passengers were either on their first cruise ever, or new to the their brands. These factors should continue to be a solid tailwind over the next decade.

Capacity

Sure, there’s growing demand, but what’s stopping cruise lines or new entrants from just building new ships and overshooting on the capacity side? Well, it can take almost half a decade to design and build a cruise ship, and there’s only a few shipyards capable of building them. Shipyards operate at pretty close to full capacity, so it would be ~2028 before a ship ordered today would be ready to sail.

Building a cruise ship is a massive risk for a potential new entrant. You have significant upfront costs and need to negotiate with shipyards for space at their dock — shipyards are incentivized to go with larger lines who offer more certainty and the opportunity for repeat business; even once you’ve built the ship, they now have a 100,000+ ton ship that requires consistent maintenance and needs to be dry docked by law every three years for detailed checks and refurbishments. For cruises to be economical, they need to be sailing at full capacity on pretty much any day that ends in a y... This is an industry with massive fixed costs and where operating leverage is crucial, new entrants don’t have this benefit.

Where new entrants have managed to make an impact is on the luxury side, specifically hotel brands launching smaller ships (few hundred passenger capacity) that are closer to yachts than a stereotypical cruise ship. Four Seasons and the Ritz-Carlton are examples of this; this shouldn’t drastically impact the economics for overall industry (capacity ~700,000), even if it could potentially pressure pricing on luxury brands.

Given the long lead time to build a cruise ship and the limited number of shipyards, additional capacity is known well in advance. Unsurprisingly, new capacity hasn’t been a priority for cruise lines over the last couple of years. All operators are focused on paying down debt and returning to an investment grade credit rating. Capacity is expected to grow ~4% annually over the next few years according to Cruise Industry News, while demand is expected to grow ~6% (using expected passenger sailings above). Fincantieri, the largest cruise shipbuilder (~40% market share), also forecasts demand to increase faster than capacity due to a lull in orders during the pandemic, this will create a supply gap by ~2026.

I think this is a great set up. You have a growing vacation alternative, a generation of wealthy baby boomers continuing to retire with time and money, all with less new capacity coming online over the next few years.

Capital Allocation

This is pretty simple. All free cash flow cruise lines generate is going to reducing leverage. Cash flow fluctuates a lot from year-to-year, depending on the payment schedules for new ships, but all major cruise lines are focused on getting back to investment grade credit status in a few years (potential catalyst). New ships, while costing capex and reducing free cash flow, create new ECA capacity which effectively allows operators to take on debt at lower rates.

One of the biggest concerns for cruise lines is their capex is always in excess of their depreciation. This is a reasonable concern and should be tracked closely. I think it’s fair to expect capex to be more than depreciation given the industry has consistently grown (outside of covid) and ships have very long useful lives — depreciated over ~30 year by most operators. Capex spend should be down over the next few years (on average) though as ship orders slowed significantly during the pandemic — Carnival, the largest cruise line with ~40% market share, is expected to take delivery of only 1 ship a year over the next 4 years (17k new capacity — avg. ~4,250 per ship).

Valuation

The three public cruise lines trade ~9-10x NTM EV/Ebitda. This doesn’t sound crazy cheap when you consider these are capital-intensive businesses… the depreciation is large and very real… But, like mentioned above, demand is growing faster than capacity which should create a favorable pricing environment, and cruise lines are still optimizing their operations after being shut down for >1 year. I think we look back in a few years and see significant earnings growth, debt reduction accruing to equity holders, and maybe even some multiple expansion in a upside scenario (investment case not reliant on this last one).

Final Word

I’m going to dive into some detail on Carnival and Royal Caribbean in future write-ups, there’s some company specific considerations like industry positioning, leverage concerns, management competence, and dilutive convertible debt that needs to be accounted for, but I think we’re still early in the cruise line recovery.

Hi Matt,

gutsy call to invest in this lousy business. Looking forward to your detail on CCL/RCL.

Tom

Great write up. Have you taken a look at Viking’s F-1?