Marathon Petroleum: A Simple Bet

Marathon Petroleum: A Simple Bet

Limited supply & structurally lower opex costs make U.S refiners an attractive bet imo. Long-term oil demand is uncertain but we're getting current free cash flow and a normalized midcycle multiple.

I recently bought some shares of Marathon Petroleum (MPC 0.00%↑ ), the largest refiner in the U.S. The thesis is relatively simple:

High probability of long-term crack spreads settling above pre-pandemic levels

Near-term free cash flow

Aggressive capital returns.

The thesis kind of fits with my U.K. housing post from earlier in the year; a cyclical business that is currently overearning and being priced as such, but the industry is either unable or unwilling to increase supply. In this scenario, the refiner is a little riskier as supply can come from outside the U.S., and demand for oil products is more volatile than housing; refiners are trading at cheaper multiples though.

Background

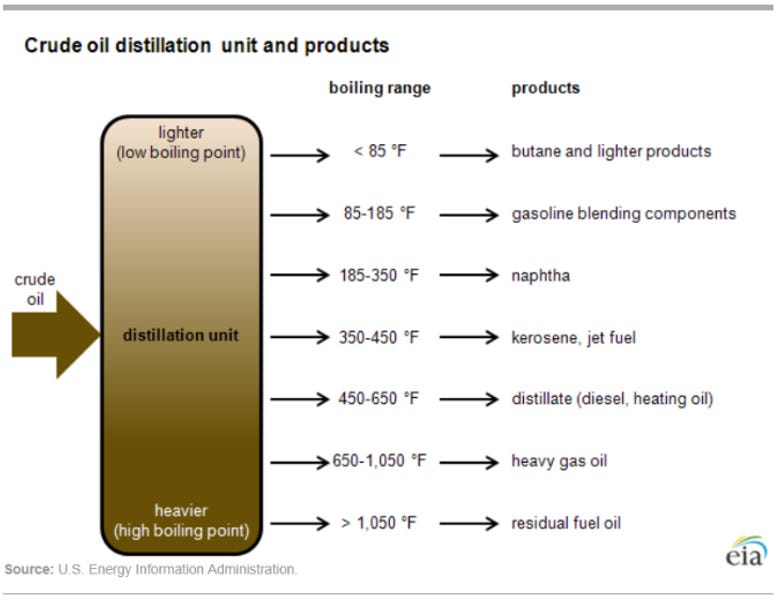

Refiners are in the business of taking unprocessed crude oil and turning it into petroleum products: gasoline, jet fuel, diesel etc. The average 42-gallon barrel of unprocessed crude oil is refined into ~20 gallons of gasoline, ~12 gallons of diesel, ~4 gallons of jet fuel, with the remaining a mixture of other products.

Refineries are complex but the high-level process is easy enough to understand. Crude oil is separated into different petroleum components through a process called distillation; the process heats crude oil until it becomes a vapor, the vapor is then fed into a distillation unit, where it is separated into fractions (petroleum components) based on its boiling point.

Heavier fractions can then be processed further into lighter (more valuable) products like gasoline. The most common method is cracking, where heavy hydrocarbon molecules are cracked into lighter ones. Finally, the output is treated and made ready for sale to the market.

Refiners get to keep the difference between the cost of unprocessed crude and the petroleum product sold to the market. This difference is referred to as a “crack spread”. You then minus the refiners’ operating costs, and you have their profits.

Current Situation

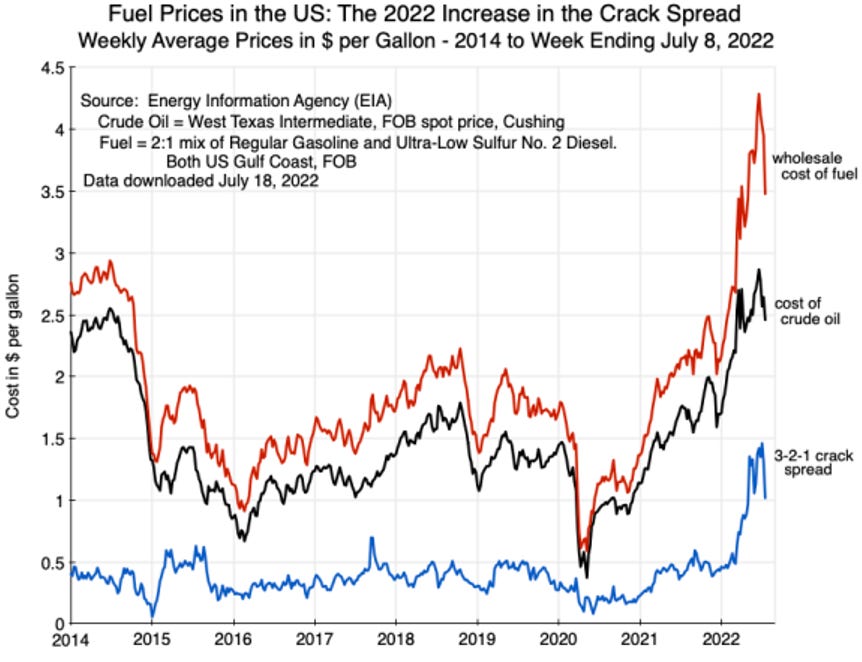

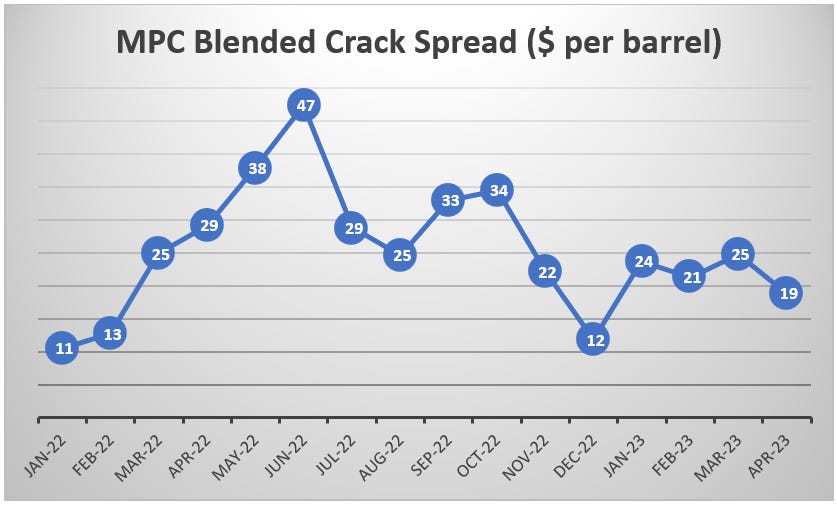

From 2014-2021, crack spreads averaged ~$15 per barrel, but in early 2022 crack spreads blew out to >$60 due to the war in Ukraine. Given that the cost of refining crude doesn’t really change that much (outside of maybe natural gas costs), margins effectively went up 4x for refiners, all in the space of a few months. Earnings have exploded since, with Marathon’s Refining & Marketing segment Ebitda jumping to ~$19bln in 2022, up from ~$3.5bln in 2021.

Crack spreads are now normalizing, with MPC’s avg. blended crack spread ~$23 in Q1 (fell to ~$19 in April), but the business is still printing cash.

There’s a little bit more to MPC’s business than just refining; they own ~65% of an MLP midstream business called MPLX (consolidated on their financials). MPC currently has an EV of ~$70bln with ~$15bln in net debt, but MPLX makes up ~1/2 of that. So, you effectively have a Refining business worth ~$35bln EV with no net debt; MPC holds ~$7bln of debt but has >$11bln in cash – most of the debt (~$20bln) is held at MPLX with no recourse to MPC.

MPC’s refining business made >$19bln in Ebitda in 2022 on a $35bln implied EV… Now this isn’t going to happen in 2023, but refining Ebitda was still ~$3.8bln in Q1 23 on a blended ~$23 crack spread. I think the situation sets up for an average return if crack spreads return to pre-pandemic levels, with significant upside if they settle slightly higher.

Let’s get to the thesis.

Crack Spreads

As mentioned above, crack spreads have been elevated over the last year but have been trending down. Long-term though, I think there are a few reasons to believe they stay elevated.

First, refining capacity isn’t increasing; 2022 capacity was right around 2013 levels (~18mmbpd), with U.S. oil consumption roughly flat over the period. Refiners are closing older facilities or converting them into renewable facilities, which typically produce less oil equivalent barrels. A new refinery hasn’t been built in >40 years in the U.S, with new capacity coming from the expansion of legacy facilities. The cost and time to build a new factory, along with uncertain long-term demand make the investment case difficult to justify. Kevin O’Leary did say he wanted to build a refinery, but the announcement was short on details and low on credibility…

Structurally lower natural gas prices give U.S. refiners a cost advantage. Natural gas is a major input into refining due to the energy required for heating crude, so operating costs can move around significantly depending on the cost of natural gas. Marathon says ~15% of their operating costs are natural gas, and a $1 move in price (mmbtu) has a $330mm impact on their Ebitda. Prices have been consistently lower in the U.S. vs Europe for much of the past decade, due to the extraction process for shale creating an abundance of natural gas; the war has only exacerbated this dynamic.

It’s hard to imagine a situation where the current supply dynamics in Europe return to pre-war levels quickly. Russia holds ~7% of worldwide refining capacity, and while this capacity hasn’t vanished, sanctions impact the volume available for European nations.

Cash flow

MPC’s refinery cash flow is volatile. In 2020, the refining operations lost ~$3.5bln, and in 2022 they made ~$9.5bln (to calculate refinery cash flow I’m taking MPC 10-K cash flow mins MPLX’s 10-K cash flow). But given the current valuation, a quarter of over earning cash flow can go a long way. In Q1 23, MPC’s refinery operations earned ~$2.4bln. Even if spreads keep heading lower, it’s not hard to imagine the refinery business generating >$5bln in 2023; add in MPC’s share of the midstream business (~$2.5bln) and we get a free cash flow yield >15% on a reasonably conservative capital structure.

Capital Returns

Cash flow is great, but what is management doing with it? MPC has found itself in the enviable position of having way more cash than the business requires. In 2021, they sold Speedway, their fuel and convenience store business for ~$21.5bln (~$17bln after tax). Then the war in Ukraine meant crack spreads exploded and MPC printed cash. Since the beginning of 2021, they’ve used this excess cash to pay ~$3bln in dividends and repurchase ~$20bln of shares. The problem? They still have ~$11.5bln in cash left.

This is obviously a good problem to have, and indications from management point to continued buybacks, with the board increasing the buyback authorization by $5bln (~$11.5bln left) in Q1; they also pay a consistent dividend (covered by MPLX distributions to MPC). Management consistently describes the business as a “return on and return of capital business“. They have invested in some renewable projects, most notably a JV to upgrade their Martinez factory to produce ~730mm gallons of renewable fuels a year (previously produced ~160mbpcd), but the projects have been reasonable from a capital intensity standpoint.

A quick point on management, the recent swings in the oil market give us a good opportunity to see how management operates during different environments. 2020 was obviously not a great time for MPC, but management openly described the market and the actions they were taking to work through the difficult macro environment (reducing utilization, cutting workforce etc.). They’ve been consistent in how they plan to operate (return on capital and return of capital) through both up and down cycles. While good management won’t change crack spreads, I feel good they’ll communicate what they’re seeing and continue to focus on returning capital.

Risks

This bet can basically be boiled down to stable demand for crude in the U.S., refining supply stays flat or declines, and natural gas prices stay lower in the U.S. vs Europe. The last two I think have a reasonably high likelihood of occurring, with demand being the most volatile and hardest to predict.

EIA forecasts U.S. oil consumption will be roughly flat for next few decades (18-20mm barrels a day). A 3-decade forecast probably isn’t worth the paper it’s written on, and with potential negative catalysts like electric vehicles adoption and renewable energy, it’s clearly a significant risk. I’m skeptical of how fast oil and gas demand will dissipate, and I’d expect refiners to react and right size their capacity as the situation evolves (warning macro prediction). What makes me comfortable with this risk? I’d point back to the 15%+ current fcf yield and 10%+ in a normalized environment; I think we’re getting offered good odds to take the risk.

Valuation

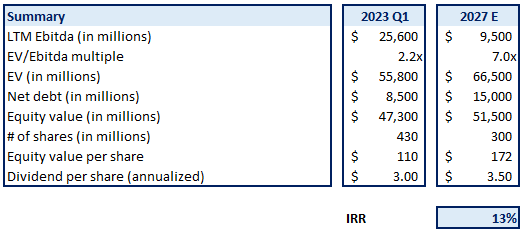

The valuation lies more in the probabilities than some elaborate DCF but I’ve tried to put a potential normalized scenario below:

MPC’s refining business has refining capacity of ~3mm bpd: ~1.2mm Gulf Coast, ~1.2mm Mid-Continent, and ~600k West Coast. If we assume $16 crack spread and $11 operating cost per barrel (incl. turnaround costs) we get ~$5 of Ebitda per barrel. ~2.8mm bpd utilization and that’s ~$5.1bln of refining Ebitda.

Midstream Ebitda was ~$5.7bln in 2022 and has a more stable earnings profile. ~3% Ebitda growth through 2027 gets us ~$6.7bln. If we then take 65% of midstream earnings that’s ~$9.5bln of MPC look through Ebitda in normalized/mid-cycle scenario.

Net debt increases to ~$15bln over the forecast period as management keeps using their excess cash to buyback stock (note I’m only including 65% of MPLX’s debt). A $150 avg buyback price on ~$20bln reduces the share count by ~130mm shares (30% reduction).

Using 7x as the multiple gets us a slight increase in EV and a similar market cap, but the buybacks mean a ~$170 share price and 13% IRR (incl. dividends). I’d argue the upside is significantly larger than the downside given the low valuation and a small increase in crack spreads translates to a significant jump in Ebitda.

Final Word

This investment is a little outside what I’ve invested in in the past and I’m fully aware I have a lot to learn when it comes to the oil space, but betting on a business that’s printing cash and is reasonably priced on a midcycle multiple doesn’t feel like a terrible bet (famous last words??).

must have done a bit of effort to compare u.s. peers, dk, dino, etc... ?

what here jumped out as most asymmetric?