Carnival Cruise Lines: 2025 & 2026 Cash Flow

Carnival Cruise Lines: 2025 & 2026 Cash Flow

Follow up to my cruise lines post. I think the market is overestimating the likelihood of demand cracking. If demand stays solid, there's potential for ~20% CAGR over the next few years.

I posted on the cruise industry a couple of weeks ago but wanted to dive into a bit more detail on the individual names (CCL 0.00%↑ & RCL 0.00%↑). This post is going to focus on Carnival, the riskier of the two but the one with the most upside. Cruise lines currently make up ~9% of my portfolio. I see a few potential outcomes from this bet:

A quick exit (for a loss) if fundamentals deteriorate and demand cracks; basically, I’m dead wrong.

Hold for a few years and sell after CCL uses their low capex intensity years, 2025-2026, to aggressively pay down debt — this probably produces the highest CAGR.

Longer-term hold through 2028.

The market is concerned CCL will struggle to reduce debt, especially if demand slows and cruise lines lose their pricing tailwind. If pricing weakens and CCL can’t grow earnings, they’ll have no choice but to issue equity to pay for upcoming debt maturities. Not great…

My bet is we see solid demand over the next year few years and CCL uses their low capex intensity years (2025-2026) to gush cash and reduce debt rapidly (the catalyst). We’ll get into more detail on this later but let’s start with some background.

Background

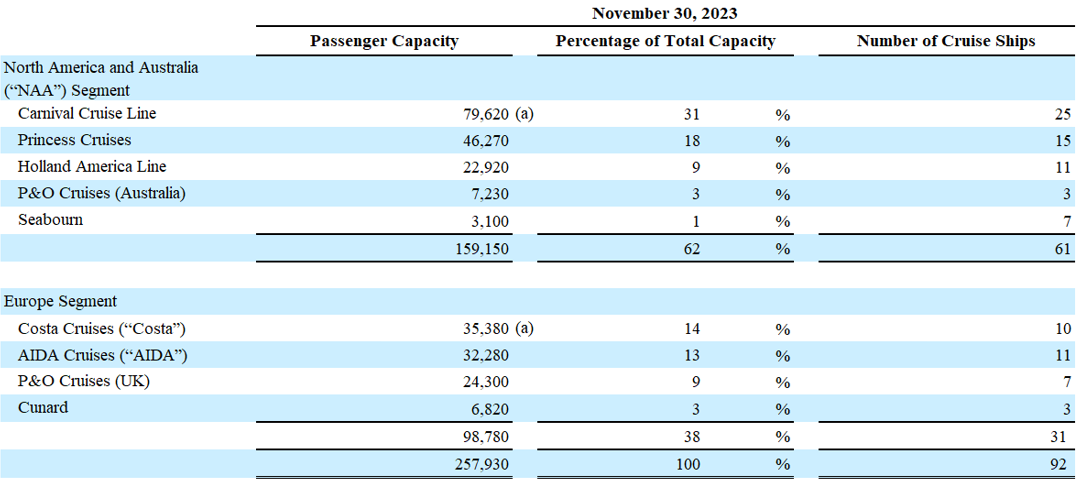

CCL is the world’s largest cruise operator, making up ~40% of the industry’s ~700k passenger capacity. They operate 8 brands and 94 ships; the largest brand is Carnival Cruise Line, with ~90k capacity and 27 ships (for simplicity I’m going to refer to the Carnival Corporation as CCL).

CCL operates across all segments of the cruise market, from contemporary (Carnival), to luxury (Seabourn). In general, CCL brands offer a value for money option in their respective categories; compared to Royal Caribbean, they generate ~20% less revenue per ALBD (Available Lower Berth Day*).

*ALBD is an industry metric for capacity (assuming 2 passengers per cabin)

~33% of CCL’s sailings are in the Caribbean, with another third in Europe (incl. the Mediterranean). The rest are in locations such as Alaska, Australia, New Zealand, and Asia.

The Situation

The cruise industry is still recovering from the pandemic. Sailings were cancelled for >500 days and CCL lost ~$25bn from 2020-2022. Historically, CCL has grown revenue and Ebitda ~mid-single-digits, generating ~$1-2bn in annual free cash flow (cash flow can be volatile depending on ship building schedule), and operated at <2x Net Debt/Ebitda. Historical P&L below:

This all changed with ~$25bn of cash burn in 3 years; CCL was forced to issue ~$25bn in debt and >$5bn in equity. They survived but are now dealing with the harsh reality of repairing their balance sheet. Ebitda in 2024 should be >$5.6bn, up from ~$4.3bn in 2023; however, with ~$1.9bn in interest expense and >$4bn in capex, it’s unlikely they make much progress in 2024.

So, how does this investment work? Ebitda is forecast to grow 30% in 2024 and cash flow is barely positive? A few things need to happen:

Solid demand

Management execution

Cash flow (2025-2026).

Demand

This one is obvious, solid demand for cruises over the next few years is needed for this to work. The market is concerned demand is driven by pandemic revenge spending (delayed for cruises due to the cancellation of sailings); I see it differently.

First, demand for cruises is rising because they’re more popular. Morgan Stanley estimates a cruise is ~25% cheaper than a land-based vacation and the quality of cruises continues to improve with bigger ships and new tech. There’s also a whole generation of baby boomers (the richest generation in history) retiring at a rate of ~10k a day and looking for ways to enjoy their free time. ~80% of those that cruise plan to do so again and the new-to-cruise mix continues to grow; this should create more recurring cruisers.

CCL has more European exposure than other large cruise lines and this has impacted their recovery. ~75% of revenue from European cruises comes from ticket sales as they spend less while onboard (North America segment is ~65%) and 2023 occupancy was only ~95% in Europe vs ~103% in North America. European unit economics will never match the U.S., but a return to historical occupancy is low hanging fruit for CCL.

Capacity growth is projected to be moderate over the next few years, with CLIA estimating ~2.5%, through 2027, and Cruise Industry News forecasting ~4%; historically, cruise passengers (demand) have grown ~5-6%, annually. CCL plans to deliver 3 ships in 2024, 1 in 2025, and 0 in 2026 (more on this later). All 3 public cruise lines are preaching moderate capacity growth as they focus on cleaning up their balance sheets.

Passenger levels are still recovering and growth during the pandemic was muted due to 38 ships being taken out of service between 2020-2022. Basically, massive supply growth (ALBDs) won’t kill pricing.

Execution

When it comes to execution, CCL has historically been a low-cost provider and the low-cost operator. They’ve done this by squeezing in more passengers per ship — Carnival carries 1 passenger for every 35 tons of vessel, vs Royal Caribbean at ~41.

Ebitda margins were ~26-29% from 2015-2019 and a return to this margin profile is likely as management regains pre-pandemic efficiencies. There’s upside here as CCL has begun to embrace the megaship trend favored by Royal Caribbean; management was slow to embrace the strategy due to concerns passengers didn’t want ships so large. This turned out to be incorrect and management has introduced a new class of ship called the Excel Class.

Excel Class ships are >180,000 tons and carry 5,300-5,400 passengers. These are >25% heavier than Carnival’s previous ships but are still ~70,000 tons lighter than RCL’s Icon of the Seas. They currently have 3 of these ships in the fleet and have 2 more expected by 2028; megaships can be up to 2-3x more profitable per ALBD than older ships (per expert call with Morgan Stanley).

The industry’s pricing strategy has also changed post-pandemic, with more selling further in advance. Traditionally, a cruise line had ~50% of their capacity sold at the turn of the year; this year ~65% of available sailings were booked at the beginning of 2024. CCL is known for heavy discounts as sailing dates close in, but the new booking curve has reduced the need for this and provided a tailwind to revenue per ALBD. This appears to be the new normal and should disproportionately benefit CCL.

Celebration Key at Grand Bahama is CCL’s exclusive on-land resort and will open in 2025; it is expected to improve the Caribbean guest experience, increase guest spend, and will also help save on fuel due to it’s proximity to Miami. CCL is spending ~$500mn on the expansion and expects ~4mn guests to visiting the island by 2028 (construction started in 2022). Royal Caribbean has seen a 15% bump in Caribbean itineraries that go to CocoCay, their private destination; I don’t think it’s unreasonable to assume a similar benefit for Carnival.

I think we will see solid demand and pricing over the next few years due to moderate capacity growth and demographic tailwinds. On the execution side there’s still pre-pandemic efficiencies that can be regained, and additional juice can be squeezed from larger ships and Celebration Key. Fuel costs are a wildcard, ~10% of total opex and not hedged, but this shouldn’t stop CCL from getting back to ~25-29% margins long-term.

Cash Flow

Cash flow is volatile due to ship building schedules; cruise lines own their ships due to favorable financing terms, reported on their balance sheet as “Export Credit Facilities”. The below slide is from the Norwegian’s 2022 investor day and lays out an example of how ships are typically financed.

Typically, ~20% of a ship’s costs is paid before it’s delivered, with the remaining ~80% due upon delivery. However, cruise lines typically get very attractive terms on ~80% of the cost of a new ship, with interest rates usually in the 2-3% range. What this allows cruise lines to do is fund their new ships with cheap debt and amortize it over 12 years. Unfortunately, the slowdown in new builds means this is actually a slight headwind. CCL has ~$2.2bn of export credits maturing in 2024 and 2025, with management estimating only ~$1.3bn being issued (i.e., they have to pay down more of this cheap debt than they’ll issue).

While this is bad news, an average of 1 new ship a year through 2026 is going to create significant cash flow. Management forecasts ~$4.5bn capex in 2024 but only ~$5.4bn in 2025 and 2026 combined (~$2.7bn average). If demand holds, CCL should generate ~$6bn of free cash flow in 2 years (~30% of its market cap), with the majority being used to reduce leverage. Potential scenario below:

I don’t think these are aggressive assumptions. I’m forecasting 2% growth in capacity (ALBD), 3% growth in revenue per ALBD, and 100bps margin expansion annually (2026 margins in my scenario are still below pre-pandemic).

If the above materializes, we’re looking at ~20% CAGR and ~$26 share price in <3 years. It feels like we’re getting paid for a scenario that is very likely to happen: demand for cruises stays solid and CCL reduces leverage aggressively in 2025 & 2026.

CCL’s EV/Ebitda multiples has fluctuated between 7-11x from 2015-2019, so I think I think 8x is reasonable.

Risks

Debt

There is some concern surrounding their debt covenants, specifically their Interest Coverage Ratio which is ~2.1x based on 2023 numbers (covenant requires 2.0x and increases half a turn for the next few years), but with Ebitda expected to grow >30% in 2024 and debt to drop materially in 2025, I don’t see this as a massive issue.

Red Sea & Baltimore port

Management has rerouted itineraries for 12 ships that were scheduled to transit the Red Sea, with most of the impact (~$130mn) in Q2. This impact was included in management’s guidance but was more than offset by ~$250mn of lower-than-expected cruise costs (excl. fuel).

The Baltimore bridge collapse is expected to impact earnings by ~$10mn as CCL moves scheduled cruises to Norfolk, Virginia; this isn’t included in management’s updated guidance in Q1 and I would bet it costs more than this — management didn’t have much time to assess between the collapse and Q1 earnings and these things tend to always cost more than a first estimate. I don’t think this impacts the thesis but they are lucky a ship was not the wrong side of the bridge.

Demand killing event

A demand killing event like the pandemic buries this thesis (shock…) and the high debt load makes it even more precarious than 2020. I think investors are placing too high of a probability of a demand killing event happening, given it’s still top of everyone’s minds; a 2008 style recession won’t be good for cruise lines but would be nowhere near as painful as another viral pandemic.

Management’s adj. free cash flow

This is one of those things that bothers me and raises questions about management. Their disclosure of adjusted free cash flow (net of export credits) is misleading.

Management is trying to show the cash available to pay for upcoming maturities as a lot of their new build costs, as we discussed above, are financed with cheap debt. But the new build capex is still a very real cash outflow and while replacing bad debt with good debt is a benefit, the adjustment is highly misleading. I would argue if you’re going to include proceeds from export credits, you should also include the required amort payments and not call the metric “adjusted free cash flow”. This isn’t a deal breaker, but I think it shows management isn’t afraid to get promotional and creative with their metrics. This is something I’ll monitor closely.

Final Word

I think CCL is a good risk adjusted bet. We’ve got to tolerate some macro risk but we’re potentially getting a 20% IRR for a base case scenario that is pretty likely to happen imo. Capacity growth is reasonably certain, pricing growth at 3% is lower than 2015-2019, and CCL’s ship building schedule is set through 2026. Management has also been clear that cash flow will be used to paydown debt (low capital allocation risk).

I think the market is overestimating the probability of demand cracking due to the recent memories of the pandemic. I admit it’s a risk, but one I’m happy to take given the potential reward.