Barratt Developments - The U.K.'s Largest Home Builder ($BDEV)

Barratt Developments - The U.K.'s Largest Home Builder ($BDEV)

In a December post on U.K. home builders, I said I'd write-up Barratt Developments. That's exactly what this post is about...

I wrote a piece a few weeks ago about U.K. home builders and how I thought the industry set up was interesting. I said I would write-up Barratt, the U.K.’s largest home builder, so that’s exactly what I’m going to do here. I’d recommend reading the previous article for background, but I’ll quickly recap key industry points before diving into Barratt.

Recap

U.K. home builders face major headwinds due to the following:

Macro

Inflation is running ~10% in the U.K. as the war in Ukraine and supply chain issues heavily impacted the economy. To combat this, The Bank of England has raised rates from near 0 to 3.5%.

The U.K. government has proposed tax hikes and spending cuts to raise ~£55bln.

Industry headwinds

New government regulations, specifically targeted at home builders, will create significant additional costs, with HBF estimating up to £20k per home.

The U.K. government plans to remove the 300k housing target and 5-year land supply requirements for Local Planning Authorities (LPAs). This is expected to make obtaining planning consents significantly harder.

The end of the government scheme Help to Buy (HtB) will price a lot of first-time buyers out of the market. The scheme allowed for a 5% down payment, with the government providing an interest free loan of up to 20% of the purchase price.

Put this together and you get a pressured consumer, increased industry regulation and the removal of key subsidies.

Tailwinds

Despite this I thought there were a few reasons to feel positive long-term:

There’s a structural shortage of new homes in the U.K.; new builds have only just covered household formation over the last 25 years.

Rational home builders are focused on profit rather than volume. This has kept land prices at reasonable levels.

Increasing advantages of scale due to regulation.

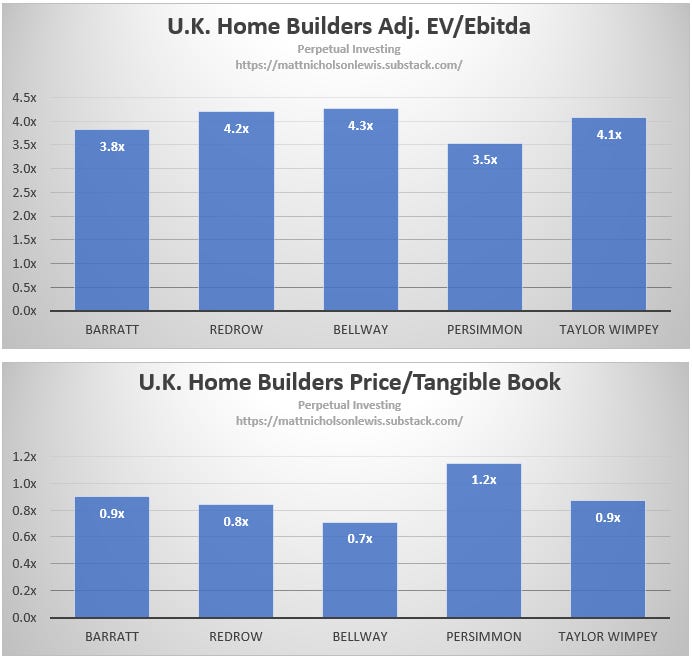

The market is pricing in the headwinds, with valuations for the industry averaging ~4x EV/Ebitda (land creditors incl. as debt) and <1x P/BV.

Barratt’s Situation

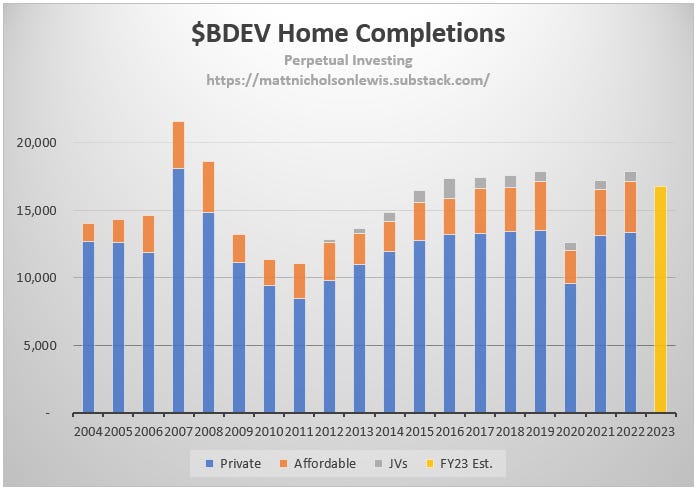

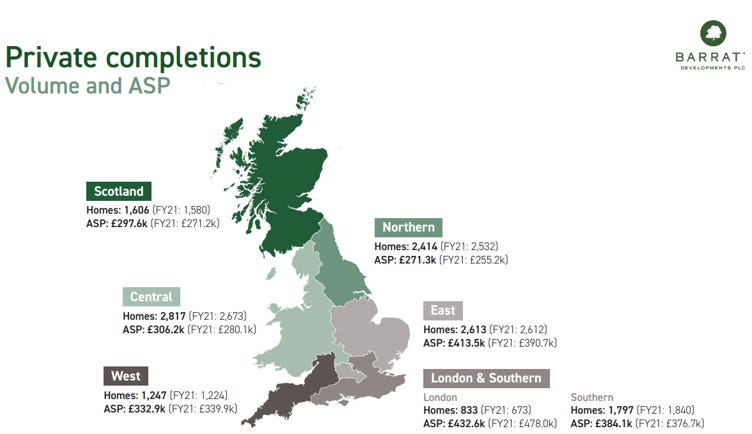

Barratt ($BDEV) is the largest home builder in the U.K. and completed ~18k homes (~9% market share) in the fiscal year ended June 30, 2022. Their build sites are spread out across the U.K., and they currently operate out of ~380 outlets.

Barratt’s recent trading update painted a bleak picture looking out over the next 18 months. Highlights from the the call:

Reported HY reservation rate of 0.44 (HY22: 0.79). This stat shows how quickly private homes are being sold per week per outlet. A bigger issue is how the rate fell throughout the period, with the reservation rate for last 3 months averaging ~0.3.

Total forward order book dropped to ~10.5k homes (~£2.5bln), down from ~14.8k (~£3.8bln).

Net land approvals were negative (290), with more plots cancelled than approved. Barratt confirmed there was no penalty for the cancellations.

Management estimated they would complete between 16-17.5k homes for the year ended June 30, 2023.

The lag between the economy and home builder fundamentals mean FY23 earnings will be reasonable for Barratt (the forward order book provides some protection), but moving forward, a 0.4 sales rate translates to ~8k private home completions a year, ~40% drop from FY22 (~13.3k).

Thesis

My thesis on Barratt centers around a few key points:

You believe the industry tailwinds, mentioned in my previous article and briefly recapped above, offset the significant headwinds long-term.

Barratt can handle an extended period of low volumes due to conservative balance sheet.

Their shorter land bank is beneficial in a low volume environment and home builders will be rational in the land market.

Capital allocation policy focused on returning cash flow to shareholders (dividends and buybacks).

Low volume

We’re going to start at #2 as the previous article and the recap hits the key points from #1. When assessing an investment in a home builder and hearing about 40% volume declines, the first question you probably have is, “can their capital structure even survive that”?

The answer to this question is yes. Barratt currently has a net cash position of ~£1bln, with £200mm of gross debt. They fund ~20% of their land bank through creditors (~£700mm), so if you include 100% of land creditors as debt, you get a net cash position of ~£300mm. For comparison, in 2008, they had ~£1bln of gross debt, £30mm of cash, and ~£550mm of land creditors.

So, the business is running with a considerable cushion and the scars from the GFC remain (cautious on leverage); but what about the expected drop in home completions over the next few years? How much operating leverage is in the business model? Barratt provides some good detail on their operating structure, which we can use run our own scenarios.

Warning: numbers incoming

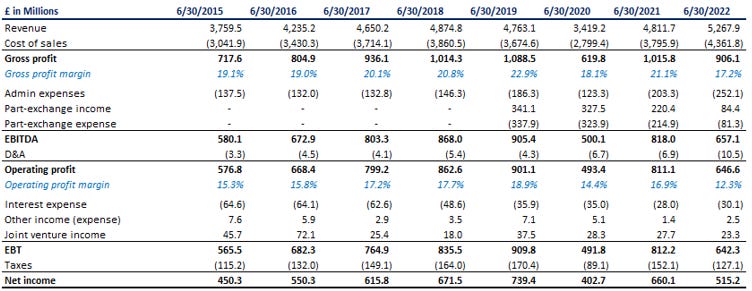

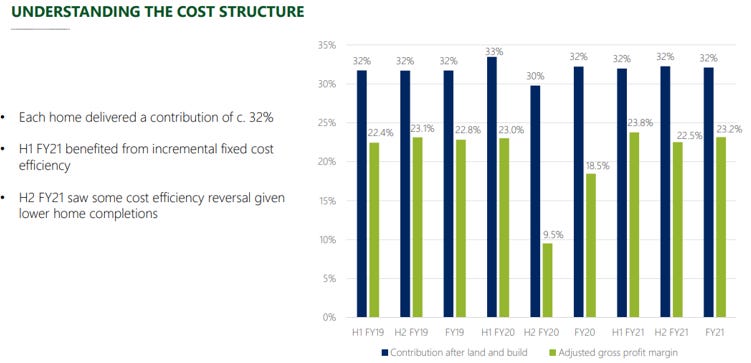

Barratt runs the business aiming for ~23% adj. gross margins, ~19% adj. operating margins, and 25% ROCE. In 2022, they hit their targets (excl. a ~£400mm adj item related to costs from the Grenfell tower tragedy – discussed in the risks section). Their cost structure is laid out nicely in the below slide.

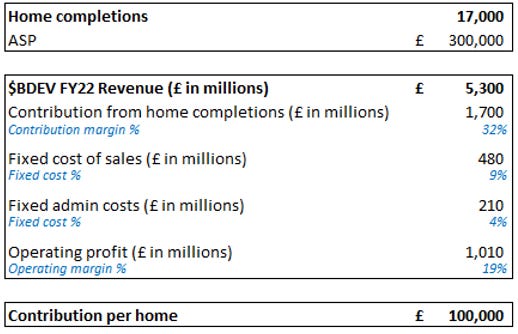

Simplistically, each home has a ~32% contribution margin (variable costs), with the remaining costs in the cost of sales line being fixed. You can include ~4% fixed admin costs as well to get to your 19% operating margin. Using FY22 as a base, the cost structure looks something like this (home completions excl. JVs):

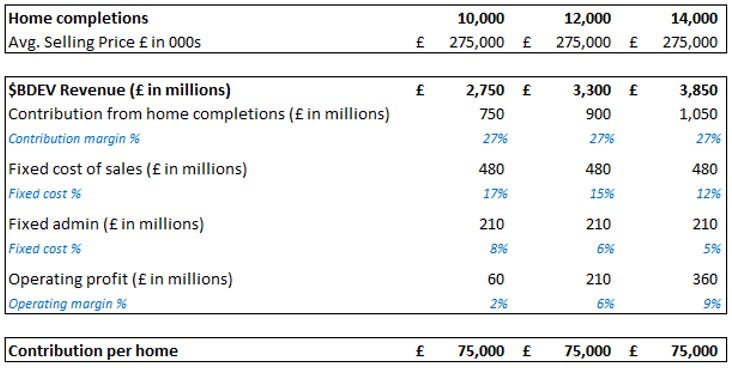

We can now effectively flex this through the P&L and choose our home completion number, along with an average selling price (ASP). I’m going to run a scenario for 10, 12 and 14k home completions for Barratt with an average selling price of $275k, and I’m going to reduce the contribution per home by £25k to account for the decrease in home prices (short-term they can’t adjust selling and land bank costs).

For the 10k scenario we’re assuming a ~8% decrease in house prices, a 40% drop in completions and assuming the business doesn’t reduce any of their fixed costs. There’s plenty of holes to be picked in these scenarios, but the point I’m trying to make is low volumes and a decrease in selling prices lead to breakeven or small losses. Not great, but with a conservative balance sheet Barratt will be around to take advantage when volumes pick back up. Compare this to the GFC where their leveraged balance sheet meant survival was the only concern (stock dropped from ~£12 to ~£0.75).

Land bank

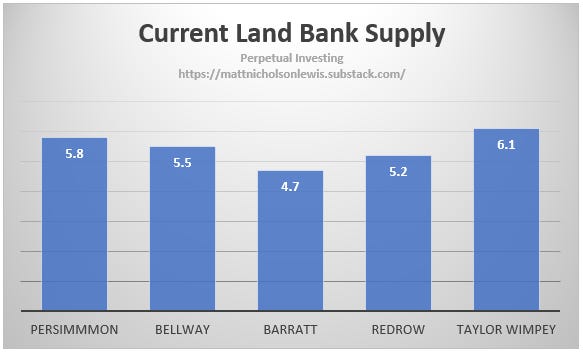

Barratt owns one of the shortest land banks in the industry (~4.5 years vs industry average of ~5.5). This can be an advantage or disadvantage depending on the market but currently, with volumes expected to decline, a shorter land bank is beneficial. As volumes drop, land bank supply increases as you’re selling less per year; not good for anyone, but better to have a shorter land bank. Additionally, a shorter land bank is better protected from a drop in home prices as you have less land, purchased at high selling price assumptions, to work through. It also means you can be first back in the market when land prices adjust.

Home builders have quickly adjusted to the new market environment and is showing, as an industry, they are rational. Home builders are price takers on pretty much every input of their business; the one area they have some control is land costs. In general, there’s not a great substitute for land sellers; sure, maybe some locations have some flexibility (e.g., commercial use) but in most cases, home builders are competing against other home builders in a land auction.

If builders act rationally, land prices should move up or down (on a lag) to a price that allows for reasonable profits. They appear to be doing just that, with recent trading updates mentioning a pull back from the land market until prices reflect updated economic reality. Some comments from homebuilders below:

“We have been increasingly selective in the land opportunities on which we have been prepared to bid, and we continue to apply our minimum 23% gross margin hurdle and 25% return on capital employed. Reflecting the changed market backdrop, we've actually seen negative land approvals in the half year. On a gross basis, we approved 16 sites for just over 3,000 plots, but we saw 22 sites for nearly 3,300 plots were moved as they were no longer proceeded.”

“As you know, by the second half, we were very cautious on the land market, both reflecting the strength of our land positions and what we saw as unattractive pricing given market conditions. This has resulted in significantly reduced land commitments in recent months, and we ended the year with a similar number of land approvals to the half year and a landbank that has reduced slightly to 83,000. This is clearly a choice which we made but one we think is right given the market conditions.”

“We're taking a highly selective approach to any new land investment and are carefully managing our outlet and work in progress position to meet current market demand… When we saw this downturn coming, we took immediate action to cancel uncommitted land deals and as a result of the actions we've taken, we now plan to open 33 fewer outlets in '23 than was previously the case.”

These quotes all say the same thing, “we are not in the land market at current prices”. I see land costs adjusting to more attractive levels over the next 12-18 months as the market adjusts to more conservative home builder assumptions.

Digging deeper, I see this adjustment being quicker in larger land sites (150 plots+), as there’s less competition. This is another reason to favor Barratt as they’re the largest home builder and focus on larger land sites. They can do this due to their size and multiple brands, Barratt Homes and David Wilson (their more premium brand); this offers more flexibility when planning and leads to better site economics.

Capital allocation

Barratt’s capital allocation has been questionable at best over the couple of decades. They bought David Wilson for ~£2.2bln in February 2007 (right before GFC), and recently spend ~£250mm for Gladman Developments, a land promoter, in early 2022. They’ve hinted that acquisitions aren’t part of their current plans and instead announced a £200mm share buyback in September. They purchased ~£100mm through the first half of their fiscal year (ended December 31, 2022) and intend to continue with the buyback in H2, despite the change in economic outlook. They also pay a dividend at a stated cover ratio of ~2x adj. EPS., which translates to ~£375mm in dividends over the last year. On a market cap of ~£4.5bln, this is ~10% of the market cap returned to investors in the last 12 months. Buybacks do increase the risk, but I don’t know a better time than when you have a low multiple, solid balance sheet, and a strong belief that volumes will come back long-term.

Valuation

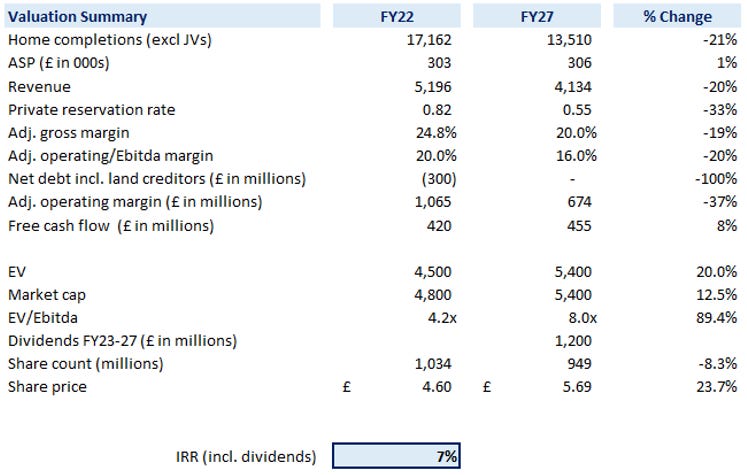

For the valuation I think it’s better to show a conservative scenario, and then explain why I think the odds are skewed heavily towards the upside. The scenario below is my best guess at a period of low completion volumes and a moderate decline in home prices, requiring the business to work through some overpriced land on their balance sheet.

I have home completions dropping from to a low of ~12.9k in FY24, with a reservation rate of 0.5 on ~360 active sites. This stays roughly flat throughout the rest of the forecast period with the reservation rate rising to ~0.55 and ~13.5k completions. I have ASP price dropping from ~£320k in FY23 to ~£305k in FY27. This means adj. gross margin falls to ~20%, with operating margin ~16%. Net debt (incl. land creditors) increases slightly from ~£300mm cash position to £0 in 2027. I’m assuming ~£300mm of buybacks through FY27 (incl. £100mm FY 23 H2) and ~25mm shares issued to account for stock comp dilution.

On the multiple, I have it increasing to 8x at the end of the period. Sounds a little stupid seeing as this is a double from the current multiple, in what I’m claiming is a “conservative” scenario, but the volatility of earnings means the multiple needs to be considered alongside Ebitda. This chart from TIKR shows the relationship between Ebitda and the multiple. High Ebitda = low multiple and vice versa.

Free cash flow is also volatile due to large swings in working capital, mainly from land investment during a given year. Assuming working capital is flat over the period, Ebitda/FCF conversion is ~75-80% (capex, interest and taxes). I’ve also included ~£500mm of costs (over the forecast period) for remediation work related to the Grenfell tower tragedy (more detail in risks section).

In my opinion, the odds skew heavily for a better outcome than this. Assuming Barratt keeps its share of the market, my scenario means ~155k industry completions in FY27, half the legacy 300k target. While it’s true second-hand homes are a near perfect substitute for new homes, home completions have only just covered household formation over the past 25 years (~150k new households vs ~175k homes built). The gap between a new home and the substitute is widening.

The blue sky scenario is lower interest rates bring back demand for housing, government assistance returns in some form, moderate increase in ASP, all leading to completions of ~18k, with margins at Barratt’s stated goals. In this scenario we’re looking at ~£1.2bln in Ebitda, a double in the stock price and 20%+ IRR.

Risks

Feel like a broken record but a lot of the risks (headwinds) were covered in the previous article (promise this isn’t an attempt to upsell you…). I’ve detailed some other risks below but the 2 key risks that would derail this thesis are: I’m incorrect about the long-term demand for housing or the land market doesn’t stay rational. Other risks that would impact returns:

The housing market experiences a massive correction, and the average selling price drops significantly. I think this is unlikely due to better lending standards (vs 2008) and the structural supply/demand imbalance in housing, but it’s a possible scenario. This will impact U.K. home builders more than the U.S., as the 30-year fixed mortgage isn’t standard. U.K. mortgages are usually fixed for 2 or 5 years, before moving to a variable rate. If rates are high a few years from now, the supply of homes could jump as people are forced to sell (jump from 3-6% rates can mean ~30%+ increase in monthly payment).

Even more regulation. One of biggest take aways from looking at U.K. home builders has been the difference in regulation between the U.K. and U.S. Regulations are extremely restrictive in the U.K. and new requirements, coupled with understaffed LPAs, means planning consents are increasingly difficult to obtain. Michael Gove has been reappointed as housing secretary (he was fired at the end of Boris Johnson’s administration) and his focus has centered around safety, rather than increasing housing supply.

Additional provisions relating to Grenfell. Barratt has booked provisions of ~£500mm relating to repair work for buildings over 11m tall, where legacy cladding may put the building at risk. This is expected to be paid for over 5 years and is separate from additional taxes the government has introduced (BSL & RPDT). Barratt is in the process of pursuing recoveries from contractors who were responsible for the issues, but it’s unlikely this is successful. The risk here is the £500mm is on the low side.

Summary

There you go, a look at Barratt and why I like the stock. Full disclosure, I haven’t actually bought the business yet as I have to get a few things sorted in my English brokerage account; little annoying as the stock is up ~10% this year already. While I like Barratt, I do feel I’m making more of a sector bet than anything else. I’m fine with that, but it does make me more open-minded to a basket approach; I’ll update the blog if anything changes in that regard.

This thesis all comes back to the shortage of homes in the U.K., millennials getting to around home buying age, and these structural tailwinds meaning profits long-term for home builders. Average age to buy a house in the U.K. is ~32, and there are ~7.5mm people currently aged 25-34 (~10% of population). Millennials (baby boomer kids) are entering that home buying age, and they need homes.