U.K. Home Builders

U.K. Home Builders

A look at U.K. home builders. Trading at ~4x EV/Ebitda, they're worth researching.

I've been doing some research on U.K. home builders (change from cable), and while I haven't invested in any yet, I think I'm at a point where I can put my thoughts on paper. Some general background info about me (feels relevant given the location of the investment), I live in the U.S. but grew up in the U.K. Don’t think it really means much but does make me more comfortable about looking for investments there.

The Situation

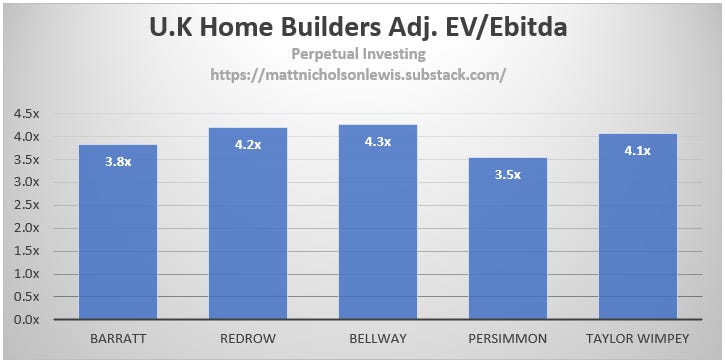

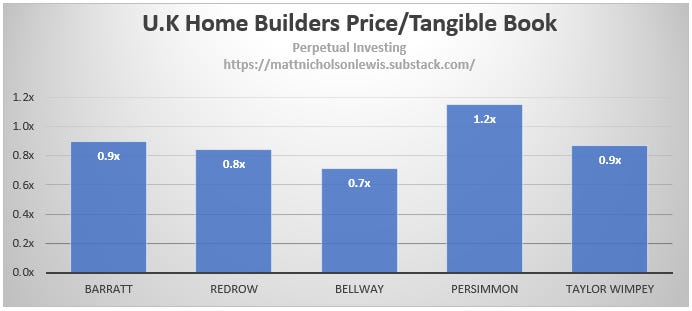

U.K. home builders trade at cheap valuations on both an earnings, EV/Ebitda, and asset basis, Price/Tangible BV; please note land creditors (amounts due for the purchase of land) have been included as debt in the EV calculations below. Book value is seen as an archaic metric, but when looking at home builders, who have real assets on their balance sheets (land), Price/Tangible BV is useful (especially as land is usually carried at cost). Home builders are also cyclical, so the first worry is getting interested in the industry right at the top of the cycle, when fundamentals are about to deteriorate but the ratios look cheap.

The answer to the question on fundamentals is they are undoubtedly going to be pressured over the next few years, due to both macro and industry specific headwinds, but how much is what I’m trying to get my head around. Let’s go over some general industry info before looking at the headwinds.

Industry

The U.K. home building industry is cyclical and usually follows the economy; with the U.K. in a recession and dealing with high inflation, the attractiveness of homebuilders has decreased significantly over the last year. The key risk home builders take is holding land on their balance sheet (usually at least 2 years) as they develop land sites into homes for sale. If home prices decrease, builders may have to take impairment charges as the land was purchased using the assumption of higher home prices.

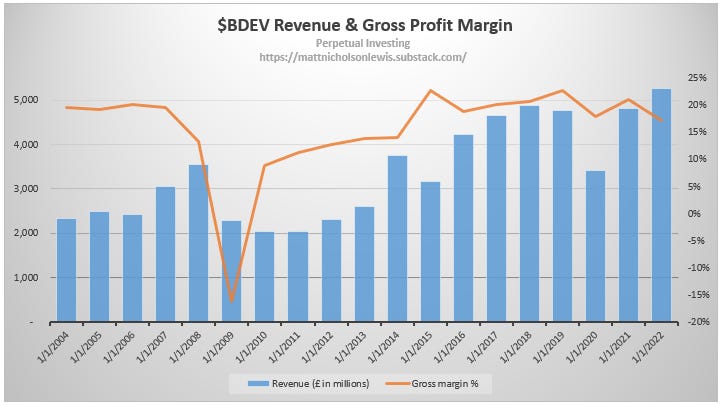

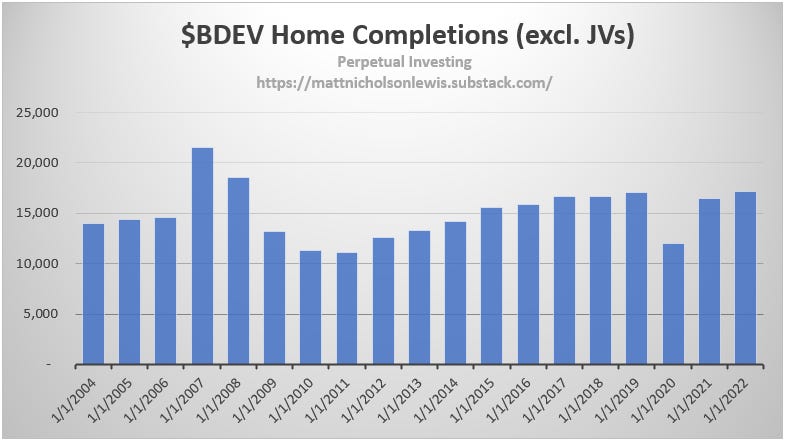

A look at Barratt’s (one of the U.K.’s largest home builders) historical revenue and gross profit margins shows the cyclicality of the industry. 2008 and 2009 had significant land impairments (2008 - ~£200mm; 2009 - ~£500mm). Recessionary periods lead to a significant decrease in revenue and a large contraction in margins. This is usually followed by conservative home builders who focus on profitability rather than growth. In Barratt’s case, home completions dropped by ~50% from the peak in 2007 to the trough in 2011, before slowly rising through the rest of the decade.

So, a bet on home builders is usually a bet on the overall economy. Barratt’s ($BDEV) stock price dropped from ~£12 to ~£1 during the GFC, and the stock is underwater over the last 18 years (including dividends the return would be positive). Unsurprisingly, investors fled home builders as the most forecast recession in recent memory manifested.

Despite the negative outlook, I still thought there were a few reasons to dig a little deeper on the industry:

A recession is already priced in, meaning valuation multiples are undemanding.

The most obvious/used comp is 2008, which is about as bad as it gets for home builders. Investors are likely pricing in a worst case scenario.

Home builders are still scarred from the GFC and have significantly better balance sheets now than in 2008 – survival for larger home builders shouldn’t be an issue.

So, despite all the red flags I decided to carry on researching… Let’s get a bit more detailed on the headwinds.

Headwinds

Macro headwinds:

Inflation – Inflation is running at ~10.7% (4 decade high) in the U.K. as the cost of gas and electricity have soared over the past year. This has significantly reduced disposable income for U.K households.

Interest rates – To combat inflation, the Bank of England has raised interest rates from 0.25% at the beginning of the year, to 3.5% at the end of 2022. Mortgage rates have risen, with the 2-year fixed mortgage rate increasing from ~2% to ~6%. Mortgages in the U.K. are typically only fixed for 2-10 years (before becoming variable), meaning the increase in interest rates will impact the majority of the U.K. housing market over the next few years (the U.S. is different due to the standard 30-year fixed rate mortgage).

Higher taxes and reduced spending – After the mini-budget that got former Prime Minister Liz Truss fired, Rishi Sunak, current PM, and Jeremy Hunt, Finance Minister, laid out tax increases and spending cuts to plug the nations funding gap. All told, this will raise ~£55bln for the government. For reference, U.K. GDP is ~£2.2 trillion.

Industry specific headwinds:

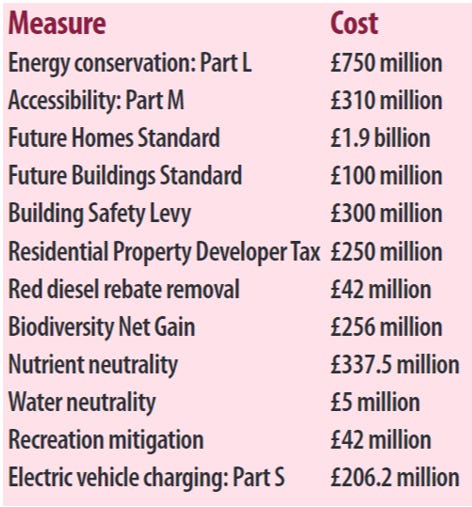

Regulation – Home Builders Federation (HBF), a representative body for U.K. home builders, estimates new regulations will create ~£4.5bln in additional annual costs for home builders (new taxes, levies and regulations); the expected cost per home is expected to be ~£20k. HBF produced a comprehensive list of regulations in the December edition of Housebuilder (page 14-15). In the interest of keeping this post a reasonable length, I’ve kept the list below to some of the major regulations:

Part L – Part L requires new homes to produce 31% less carbon emissions than the previous standard. This is expected to be achieved by slightly thicker walls and the use of more efficient fabric. This is an interim step on the way to the Future Home Standard which comes into effect in 2025 (see below). Est. cost ~£750mm.

Future Home Standard – Requires CO2 emissions to be ~75% lower than current standards. Homes will need to be “zero carbon ready”. Fossil fuel heating will be banned, with heat pumps expected to replace gas boilers. Est. cost ~£2bln.

Nutrient Neutrality – Nutrient Neutrality aims to offset damage to the U.K. water supply – specifically higher concentrations of nutrients such as phosphorus and nitrogen. If the concentration of certain nutrients in rivers gets too high, it can harm wildlife in the river catchment area. In order to secure planning permission, developers must show their work will not increase the nutrient levels. This has held up the approval of ~100k homes already. Est. cost ~£350mm.

Building Safety Levy (BSL) & Residential Property Developer Tax (RPDT) – The Building Safety Levy is currently in the consultation phase, but the goal is to raise ~£3bln over 10-years to fund the “remediation of cladding in buildings over 11m in height”. This is in response to the Grenfell tower tragedy in 2017 and is designed to protect taxpayers and leaseholders from paying to fix cladding issues. RPDT is also to remediate cladding issues related to Grenfell and came into force in April 2022, with a 4% surcharge on trading profits from developers making >£25mm. The surcharge is expected raise ~£2.5bln over 10 years (developers are rightly skeptical of the current “temporary” tag on BSL and RPDT).

Full list of estimated costs related to new regulations:

Planning Consents & removal of 300k housing target – Obtaining planning permission is often cited as the biggest headwinds for property developers. Under resourced Local Planning Authorities (LPAs), increasingly complex approval processes (e.g., nutrient neutrality), and overcoming the pandemic backlog mean planning consents are unpredictable and not being approved at the rate required. The removal of the 300k new build housing target and the required 5-year land supply from LPAs has builders worried that consents will be even harder to obtain in the future.

Help to Buy – HtB is a government scheme that has been around since 2013. The scheme helps buyers of new build homes, with the government providing an interest free loan for up to 20% of the purchase price, and only requires the buyer to put down 5% of the purchase price. This removed a significant hurdle for home buyers and made new builds more attractive compared to second-hand homes (which the scheme did not cover). The scheme ends in early 2023 and removes a key tailwind for home builders. Home builders have rolled out a scheme to replace HtB called Deposit Unlock, but this is not government funded and requires new home builders to take on additional costs (insurance) to protect mortgage lenders.

These are significant headwinds, and the current fundamentals are going to deteriorate significantly over the next few years. Sales rates have slowed, industry wide, and while fundamentals will be okay for the next 6 months due to the inherent lag in the business model, they’ll reflect the current business environment within the next year or so. So, why do I still think U.K. homes builders are interesting (fair question)? That’s where we’ll go next.

Industry tailwinds

There are three key tailwinds that I think could help the industry overcome the significant headwinds described above:

Structural imbalance between the supply and demand for new homes

Scale and control of largest cost (land purchases)

Rational home builders still scarred from 2008

Supply/demand imbalance

There is a structural shortage of housing in the U.K; the numbers show this:

There are ~28mm households in the U.K.

The average age of a U.K. house is ~60 years old.

The rate at which houses should be replaced is open for debate but using 100 years, the U.K. would need ~250-300k houses built each year to be building at a rough replacement rate (right around the previous government target).

Since 1996 there’s been an average of ~175k houses built, while the number of households has increased from ~24-28mm (increase of ~0.7% CAGR or ~150k new households a year).

Going back to 1949, the new home completion average is ~240k due to ~10mm homes built from 1950-1980. This means a significant amount of the U.K. housing inventory is >40 years old.

Demand for homes should stay elevated as millennials continue to marry and start families. It’s true that home builders compete against second-hand homes (a very good substitute), but housing inventory is aging, and new builds have only just covered household formations over the last couple of decades. The demand for housing is there long-term, even if the current economic situation keeps demand lower in the short-term.

Scale advantages and land costs

The benefits of scale in the industry are increasing for a few reasons. First, increased regulations require more scale to spread the costs of redesigns for regs like Part L, Future Home standard, and nutrient neutrality (see above). Additionally, competition for small land sites is very high, with better economics available for larger land sites (500+ plots). Larger home builders can take advantage of this discrepancy as they have the ability to develop larger sites. A quote from Colin Cole, CEO of Lioncourt sums it up nicely,

Rational home builders

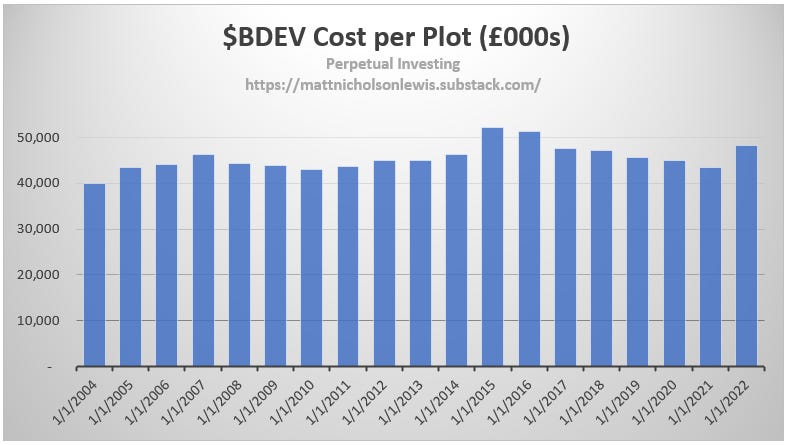

Home builders still bear the scars from 2008 and have stayed relatively cautious over the past decade. Most are run in a net cash position (even when including land creditors as debt), which gives them plenty of flexibility to work through a period of reduced demand and potential land impairments.

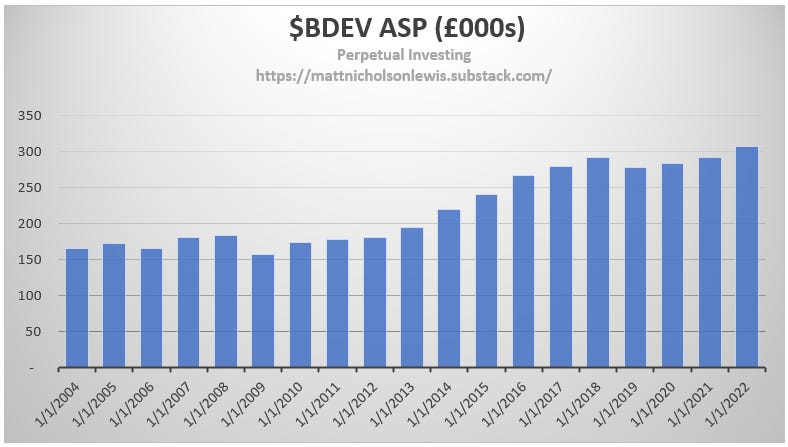

Additionally, despite operating in a cyclical industry and being price takers, they have some control over the price they pay for the land, their most significant cost. They compete with other home builders for this land, but as a group they all appear to be behaving relatively rationally. Barratt’s cost per plot, shown below, has stayed relative flat over the past couple of decades as their average selling price has increased from ~£165k in 2004 to ~£300k in 2022. It’s true that other costs have risen significantly over this period due to regulations (this difference hasn’t fallen to the bottom line), but the focus by the industry on maintaining a solid gross margin (~20%+), should help keep the industry profitable.

Summary

This feels like a classic value investor type opportunity. You have an industry priced at an extremely attractive valuation due to some very strong headwinds. I agree the headwinds are there, but trying to think about the industry 5 years out, I see the potential for reasonable margins and solid financial performance. I’m still researching but will probably write-up Barratt at some point soon (with a valuation). I haven’t pulled the trigger, but I see a potential bull case similar to oil – businesses found religion and decided not to increase capacity (drill for oil), and instead maximized cash flow with what they have. I see a different but similar situation for U.K. home builders – Disciplined land purchases (by the industry) keep land values at levels needed to deliver reasonable margins over the long-term. I still need to go deeper here but I think it’s interesting. Thanks for reading, please like and share if you enjoyed.