Nintendo Deep Dive (NTDOY)

Summary

Nintendo plans for their next gen console to build off their current 100+ million userbase.

Nintendo has several tailwinds that will continue to drive margins higher.

Their world class IP provides optionality on the upside and gives protection to the downside.

I’m long NTDOY.

* Please note all figures have been translated to USD and reference to years reflects NTDOY’s fiscal year end (March 31).

The Situation

Nintendo is either at the peak of a classic console cycle or undergoing a transition that will allow their next gen console to retain a significant portion of their 100+ million Switch userbase. If successful, it will create recurring revenues and move them away from their previous business model, where they had to reacquire every customer after a new console release. Additionally, growth in digital sales, Switch Online, and third-party developers will drive margin expansion.

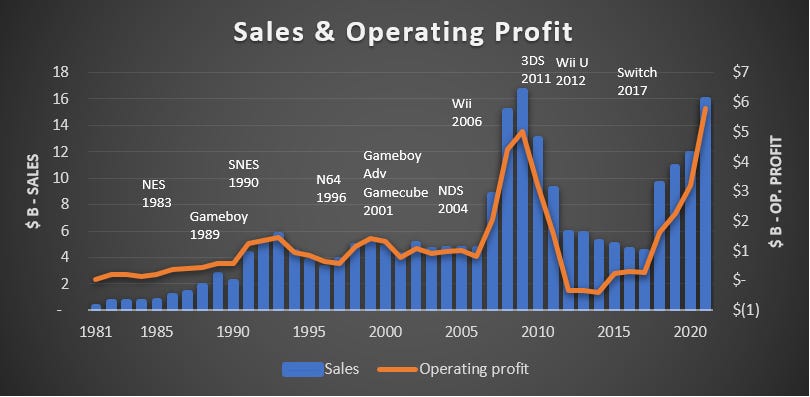

A simple chart best explains Nintendo’s past and current inflection point.

A hit console like the Gameboy, N64, or Wii and revenue skyrockets. Profits jump even further with the inherent operating leverage in the gaming business (selling incremental games costs very little). Good consoles drive demand for games and the flywheel spins, allowing them to gush cash during good times. A poor console results in the inverse, with the Wii U release in 2012 a classic example; fail to deliver a popular console and you’re in for 5+ years of pain. This boom bust cycle leads to Nintendo holding a significant amount of cash with no debt (conservative balance sheets are also common in Japan). It also makes it a difficult business to assess; you’re trying to guess if the next console will be a success or a flop, and that question is pretty much impossible to answer ahead of time. Nintendo (NTDOY) has a market cap of ~$60 billion, a net cash position of ~$10.5 billion, trades at ~9x EV/EBITDA, and ~14x cash adjusted P/E. Below is a snapshot of their financial history.

The current console, the Switch, has been a huge success. Released in 2017, the Switch now has an installed base of over 100 million and demand for the product is still strong. This thesis is built on the belief that the next generation of consoles will build off this existing userbase, and the product cycle will last until ~2024. If this is the case, Nintendo should be able to consistently grow earnings by retaining their userbase and expanding margins. I’ve detailed the key reasons why I think this will happen below:

Backwards compatibility for next gen consoles is highly likely, allowing Nintendo’s next console to build off the current userbase.

The industries move to digital sales allows for significantly higher margins as the physical retailer is removed.

The launch of Nintendo Switch Online (and Expansion Pack) will create significant recurring revenue. Releasing legacy games from previous consoles will help drive subscriptions and create sticky users.

Game development has become more cross-platform friendly, making the Switch a more attractive console to developers. Third party games are high margin and low risk for Nintendo.

Thesis

Backward compatibility

Previous Nintendo consoles tended to be backwards compatible with the previous generation. The Wii U could play Wii games and the 3DS could play regular DS games. The Switch bucked this trend, opting not to allow backwards compatibility. This was due to the Switch being the first handheld/home console and using a new type of cartridge. Due to the small Wii U installed base (~14 million sold), this wasn’t a big issue for Nintendo, even if annoying for Wii U users.

The Switch, however, has been a huge success with over 100 million units sold, so not allowing for backwards compatibility would be a huge sacrifice. Additionally, Nintendo Switch Online has ~32 million people signed up, so Nintendo has a large incentive to keep this ecosystem functioning with the next gen console (whenever that may be). During their Q3 FY22 earnings release, Nintendo management gave a hint that this would be the case:

Nintendo management are usually tight lipped about future plans, so what might feel like an offhand comment is actually a significant hint about their strategic direction. This is good news for people hoping Nintendo breaks the classic boom bust console cycle.

While based on rumors, the credibility of the leaks warrants a mention. The recent Nvidia leak exposed information that details Nintendo’s work on their next gen console. The console will be a huge leap forward, with its own customized chip from Nvidia improving frame rates and allowing for games that support 4K. I’ve linked to a YouTube video that gives some additional background. If true, the next console release (Switch Pro or next gen console) is more than what users were expecting and is another positive sign.

Digital sales

The transition to selling games from digital stores has been great for console makers’ bottom lines. Console and game developers have historically given up a significant chunk of the gaming pie to avoid the costs and operational headache of running a brick-and-mortar distribution channel. The structural shift to digital purchases effectively gives console manufacturers this portion of the pie back. Game developers such as EA and TTWO now generate >80% of their sales digitally, and the assumption is this will eventually go to 100% (at some point, a physical option just won’t be worth the cost).

Nintendo has been, unsurprisingly, the slowest mover. Digital sales have been growing, from ~15% of software revenue in 2017 to ~43% during FY 22, but still significantly lag competitors. The growth of Nintendo Switch Online and Nintendo Account will close this gap by funneling customers towards their digital store. I expect digital sales to continue growing as a portion of overall software sales.

Quantifying the transition to a digital store will help show the impact on Nintendo’s margins. On a classic $60 game, Nintendo can collect ~$17 more per sale if a customer purchases through the Nintendo Store, nearly double the margin of a physical sale. This is due to the retailer not taking their ~20% cut (~$12), and Nintendo not having to manufacture a disk and ship it to retail locations (~$5). While there are costs to running a digital store, most of this margin will accrue directly to Nintendo as they won’t reduce price and will now own the customer relationship and distribution channel.

Nintendo Switch Online

Nintendo Switch Online (NSO) was launched in September 2018 with an annual fee of ~$20. While Nintendo has had online operations in the past, they’ve finally leaned in, with online monetization becoming a larger part of the Switch strategy.

This was confirmed by the launch of Nintendo Switch Online + Expansion Pack (October 25, 2021), a more comprehensive offering that costs $50 a year and includes more content than the NSO. While there have been some criticisms of the $50 price tag, the offering is less extensive when compared to Xbox Game Pass or PlayStation Now, the value is only going to grow as Nintendo rolls out more content. Nintendo also has a couple of advantages they can tap into with their online offering:

1.) Control over content

A significant amount of their content is first party, giving them control over what to launch and when. A great example of this is the recent release of DLC content for NSOEP members. Mario Kart 8 Deluxe (43-million-unit sales) and Animal Crossing: New Horizons (38-million-unit sales), the top 2 selling games on the Switch, both have downloadable content available for free when signed up for NSOEP. You can buy the DLCs separately, but buying both would equal the price of an annual subscription (~$25 for each DLC).

2.) Legacy content

They have a large library of legacy content they can repurpose and release to drive sign ups. Nostalgia is a powerful feeling and giving customers the ability to jump back in time and play their favorite legacy games will add something unique to the online experience. Nintendo is doing just this, first with the release of certain NES and SNES games on NSO, before releasing certain N64 and SEGA Genesis games for NSOEP. I expect popular legacy titles to consistently trickle out and help drive subscriptions.

As of September 2021, NSO had ~32 million sign ups, ~30% penetration on the Switch userbase. I think Nintendo can continue to grow this revenue stream as they increase subscription numbers and move customers over to NSOEP. If we assume current revenue run rate for Switch Online is ~$640 million (32 million * $20), growth to ~50 million users over the next few years and an average annual price of ~$35 gets us ~$1.8 billion in high margin recurring revenue (I think there’s potential for 80%+ penetration long-term). This is an oversimplification as family accounts distort the numbers slightly, but the point stands, online will be a significant recurring revenue stream. It will also help retain customers when Nintendo releases their next gen console.

Third party developers

Before jumping into the key structural change in the developer market, the first thing to understand is how Nintendo accounts for third party software revenue. Nintendo takes ~30% of a third-party developer’s selling price and records this in their accounts at net revenue (their take rate). Their first party games are recorded as gross revenue, so comparing first party sales directly to third party sales in the annual report isn’t a great comparison. This 30% rate is ~100% margin for Nintendo, so increases fall straight to Nintendo’s bottom line. Adjusting Nintendo’s third-party revenue to get to an estimated gross figure, shows this revenue stream has increased from ~25% of software sales in 2017 to ~45% in the current year (when comparing gross vs gross).

Now for the industry changes. Previously, consoles had their own development engines. This meant game developers had a choice, which console was the best to create for, had the most users, and would generate the most return? The answer, invariably, was PlayStation and/or Xbox; they had large userbases and were focused on developing consoles, allowing third parties to create games (recently they’ve placed more of a focus on game development). Nintendo consoles were an afterthought, not worth the time to redevelop as Nintendo was also a game developer, meaning they were focused on selling their games first.

Over the last decade, the rise of cross platform game engines, such as Unity, has significantly reduced the cost for developers to create games for multiple platforms. Nintendo is the main beneficiary of this change as they were historically the odd one out. Additionally, the popularity of the Switch has inherently increased the value proposition to developers. I’d expect continued growth of third party revenues, even if at a more modest pace than previous years.

Summary

Putting this altogether, we get a console that is 5 years old and still going strong, a business that plans to build on their established userbase, is growing digital sales (high margin), online subscriptions (high margin), and is increasingly developer friendly (high margin). Gross margins have already increased from ~41% in 2017, to ~55% in 2021, but I see margins expanding further as these revenue streams continue growing.

Nintendo has other areas that offer upside optionality, but for the sake of keeping this pitch a reasonable length I’ll bullet them below. Most of these points are based on Nintendo’s recent willingness, under President Mr. Furukawa, to utilize their world class IP (difficult to quantify but provide asymmetric upside skew):

Nintendo is a world class game developer that has consistently delivered family friendly games for decades. They’re not afraid to try new ideas, and they will continue to churn out innovative games.

U.S. activist investing firm ValueAct Capital has a ~2% stake (purchased in early 2020). Their presence has helped push Nintendo to speed up monetizing their IP and even initiate a share buyback.

Moved into visual content with the announcement of Super Mario Bros movie (holiday 2022 launch) and nominated Chris Meledandri to the board (producer of Despicable Me). Nominating Mr. Meledandri hints that Nintendo plans to release more visual content in the future.

Nintendo World in Japan, Osaka, inside Universal Studios. While the opening was not well timed (pandemic), theme parks based on world class IP have proven successful.

Potential of the mobile product and growing use of microtransactions. Still reasonably conservative in their use when compared to other developers (e.g. EA).

Potential outsized growth opportunities in Asia (outside Japan). Switch partnership with Tencent in China, while hindered by China’s crackdown on gaming, still has significant potential given current small base. Sales started in December 2019 and they sold ~4 million consoles during 2020 (3 million of these were on the grey market).

The video game has secular tailwinds with gaming becoming more popular. This was highlighted by NPD ’s recent data showing older age groups are gaming more regularly.

Risks

1.) Console cycle

The key risk to this thesis is Nintendo can’t move away from the console cycle they’ve been beholden to since the launch of the NES in the 1980s. I’ve detailed why I think they can above, but if I’m wrong, the valuation will rerate lower, and the question will be whether they can reacquire their userbase. For reference, 2015, during the height of Wii U disaster, the market cap was ~$20 billion. Given some of the structural changes and quality of the IP I think it’s unlikely its falls to this level again, but stock prices can do anything when investors become fearful.

2.) Consistent underwhelming game launches

I consider this highly unlikely due to Nintendo’s long track record of producing world class games but must be mentioned given the potential impact. An extended period with underwhelming software releases will significantly reduce time played. This will ripple throughout the rest of their business lines as popular software games drive the rest of their IP.

3.) Performance falls too far behind PlayStation and Xbox

The leaked Nvidia rumor helped reduce the risk that Nintendo falls too far behind Xbox and PlayStation in the power of their console. While keeping within a reasonable range is required for the performance of games, Nintendo isn’t competing with PlayStation or Xbox on graphics.

4.) Conservative management

Management has historically been very conservative in managing the business outside of gaming. This has led to them missing out on significant opportunities to monetize their IP and resulted in frustration from investors. While they’ll likely never get as aggressive as American companies (e.g. Disney), management has begun to get more comfortable with this concept. Visual content, mobile, theme parks, and dedicated Nintendo stores should continue to spread their IP outside of their gaming channel.

This conservatism translates over to their financial profile, Nintendo holds no debt and ~$10.5 billion in cash. While a takeover is out of the question, since ValueAct has been involved, management has initiated a buyback of ~$860 million during the current year, retiring ~1.5% of Nintendo’s outstanding shares. An investment, however, must accept and account for the fact that Nintendo will never be run like a U.S. firm.

5.) Semiconductor shortage

A continued semiconductor shortage will increase the cost of the Switch and could put some pressure on margins. The larger risk would be a prolonged shortage that delays Nintendo’s next gen console launch or puts them in a position where they can’t meet demand when they launch. Given the success of the Switch and its continued popularity, a longer than usual life cycle is already confirmed, giving them some flexibility when it comes to the console release timeline.

6.) Cloud gaming

A longer-term risk, but cloud gaming has the potential to completely upend the console market. This is where Nintendo’s primary focus on game development reduces the risk that cloud gaming removes the need for consoles. In fact, Nintendo would probably benefit from being forced to move on from the hardware portion of their business, as it would open them up to sell to their everyone.

7.) Currency and ADR

As NTDOY is an ADR so we’re subject to exchange rate and political risk.

Valuation

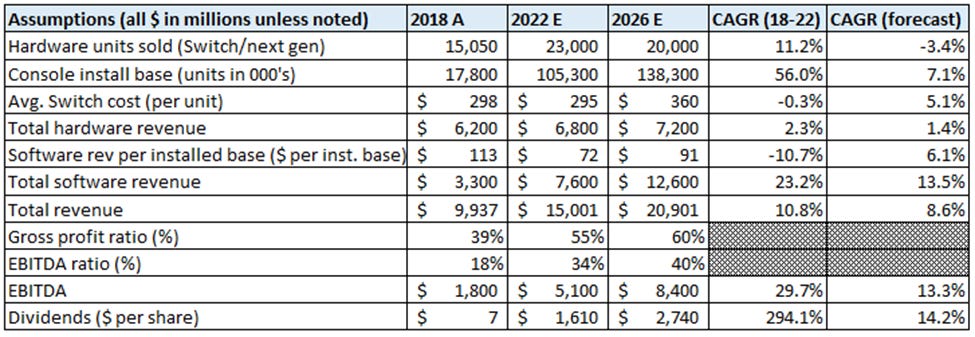

Now to try turn all this into a valuation. Nintendo is difficult to value due to historically volatile earnings and the likelihood of a new console before the end of FY26 (end of the forecast period). I’ve detailed a potential scenario below but a valuation here is more art than science.

Hardware

I’ve estimated that ~20 million hardware units sold annually through 2026 (80 million total) with an avg. cost of ~$360 in 2026. I’m guessing we’ll get a new console in FY24 which will drive the increase in average cost and continued demand for hardware. I’ve then estimated that from 2024, 75% of consoles sold will replace an existing Switch user. This means that 20 million console sales will increase the installed userbase by 5 million (I’m using 10% pre next gen console release). This gets us an installed base of ~138 million and ~$7.2 billion of hardware revenue in 2026.

Software

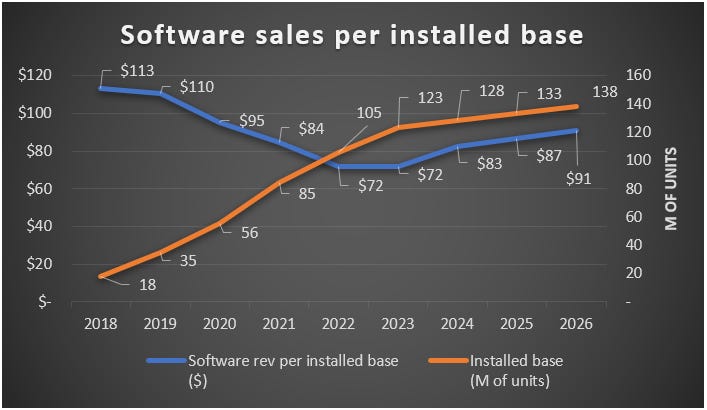

In Q4 2019, Mr. Furukawa introduced a new method to track Nintendo software performance. Due to the growth of Switch online and DLC, the old “Software Attach Rate” metric (software units sold/hardware units sold) had become less relevant, and instead, “Sales per Hardware Unit” was introduced (software sales/installed base).

This change makes sense given the growth of revenue streams like Switch Online, but the new metric has moved around as the installed base has matured. The chart below assumes a more stable installed base throughout the forecast period, resulting in Sales per Hardware Unit increasing as the next gen console is released.

Margins

I’m predicting the increase in high margin revenue will allow Nintendo to increase gross margins from 55% in 2022 to 60% and EBITDA margins from 34% to 40%, by 2026. This is driven by digital sales, online, and third-party sales all being high margin products (discussed above). R&D spend has been on the rise and will continue to rise through 2026 (I’m predicting $1.25 billion in 2026, up from ~$850 million in 2021). Margins can move significantly depending on sales, so a bear case scenario will lead to a significant contraction in margins.

Other

Nintendo holds a bunch of investments (worthy of their own write-up) that are hard to quantify due to their accounting treatment and lack of disclosure. These include a 30% stake in Pokémon, a 10% stake in the Seattle Mariners, and a number of minority investments. These aren’t included in EBITDA estimate below. However, it’s probably fair to question whether 100% of the cash (~$20 billion in 2026) should be included in the EV calculation as they’re likely always going to carry a large cash position. I’m going to assume $0 investment value but include 100% of the cash position in the EV calculation for the sake of this (very rough) valuation attempt.

Summary

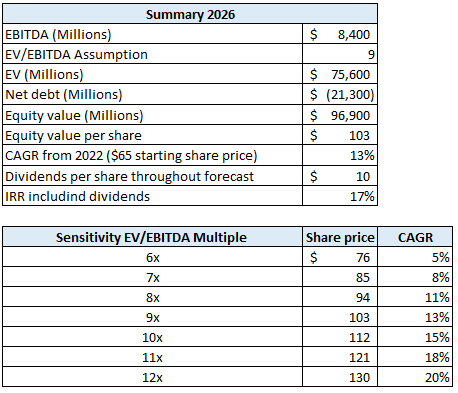

A base case, assuming a 9x EV/EBITDA multiple (I’d argue there’s potential multiple expansion if they successfully make the transition), would give us a ~$105 stock price and ~$10 of dividends received (1/3 of operating profit) over the investment period, an IRR of ~17% through FY 26.

A potential upside scenario would be margins expand even further, potentially a ~44% EBITDA margin. Leaving all other inputs the same and increasing the multiple to 11, this would result in an IRR of ~25% ($135 stock price and $11 of dividends).

A downside scenario would be a difficult transition to the new next gen console and a breakdown of the thesis I’ve detailed above. I’d argue the IP and heavy cash position set the business up to weather this storm, but using the Wii U situation as a proxy, we’re looking at a ~50% drawdown if thesis breaks down and next console is a flop. I’d assign significantly higher probabilities to the upside and base case than the downside though, which is why I’m long.

Conclusion

The current price of Nintendo includes a risk premium for a potential failed console transition, and with the Wii U disaster still in the back of investor’s minds, this allows for an attractive entry point. There is uncertainty around the console transition, but I think Nintendo’s IP and their willingness to monetize it can act as floor on the stock in a downside scenario. While I’d take the valuation work with a pinch of salt (it’s admittedly very rough), I think Nintendo offers an attractive risk/reward bet at current prices. Thanks for reading.