Is it Time to Consider Airlines?

Is it Time to Consider Airlines?

Air travel demand has rebounded and stocks are up this year, but I think the market might be underestimating the outlook for airlines.

I would love to successfully invest in an airline. Unfortunately, successful investment and airlines have, historically, been mutually exclusive. I’ve been getting that itch again and I’m (worryingly) starting to convince myself there’s an opportunity.

The history of airlines is well known, they’ve never really made any money… U.S. domestic passenger carriers lost ~$60bln from 1980-2010, this is despite Revenue Passenger Miles increasing from ~55bln in 2000 to ~90bln before the pandemic. The industry is just brutal:

Passenger choice is mainly determined by price (loyalty is hard to create).

Increases in demand have led to corresponding (or larger) increases in capacity – from either incumbents or start-up airlines.

They must consistently negotiate with unions, who come for any profits (salaries make up ~20-25% of operating costs).

Volatile oil prices lead to huge swings in fuel costs, which make up ~20-30% of operating costs.

Operating a network is extremely complex and only errors are remembered by the customer (no one remembers your flight to Chicago that arrived on time – they remember the 10-hour delay on the way home though...)

You’re at the mercy of macro events like terror and pandemics.

So why look deeper? Airlines appear to be bad businesses that have consistently proven they can’t make money. Well, I think airlines were starting to show that consistent profits were possible in the 2010s, until a once in a lifetime pandemic decimated the industry. The industry is still trading ~20% lower than pre-pandemic, with a brighter outlook imo.

The 2010s

The 2010s created a few key tailwinds for airlines. Number one was a significant amount of consolidation post GFC; Delta/Northwest in 2008, United/Continental in 2010, and American/US Airways in 2013 significantly changed the market and meant four airlines had >70% of industry capacity. Smaller players could still enter the market with low-cost financing available (ZIRP), but the size of the big 4 meant industry capacity could be managed to levels that produced profits (large carriers were willing to give up a little share to keep capacity in check).

The second half of the 2010s also had a relatively accommodative oil environment, with prices from 2015-2020 rarely >$80. This led to ~20% Ebitda margins and significant free cash flow (Delta generated ~$35bln of operating cash flow from 2015-2019).

Additionally, the continued growth of rewards and credit card partnerships gave airlines a consistent cash generator. American Express, Delta’s largest partner, paid ~$5.5bln in 2022 for miles to use with their credit cards. Credit card companies value these rewards as they drive sign-ups, and airlines create customer loyalty and receive a consistent stream of cash (Delta has a great presentation on their rewards program as part of their SkyMiles debt deal in 2020).

So, investors began to think ~20% Ebitda margins and low/mid single-digit revenue growth was reasonable long-term. Airlines were trading at >10% free cash flow yield, which compensated them for the inherent macro risk airlines carry (terror, pandemic etc.).

The pandemic obviously ended this thesis by destroying travel demand in a matter of days, but I think looking back with the information investors had at the time, it was a rational and reasonable bet to make; how quickly a lot of these investors exited their positions shows they understood the change in odds (even if they took a decent sized loss). The one area I’d push back on the pre-pandemic thesis is that low oil prices were potentially overstating earnings, some normalization was probably inevitable there.

The Pandemic

The pandemic was obviously a terrible scenario for airlines, with air travel demand going to pretty much 0 overnight. The big 4 airlines lost ~65% of their combined market caps, with bankruptcy on the table until the government jumped in with assistance. Airlines went into full cost saving mode, scrapping and storing planes, offering pilots early retirement, and avoiding taking delivery of new jets. In 2020, the industry lost ~$137bln.

Demand began to bounce back in 2022, but airlines and their supporting infrastructure couldn’t keep up. The industry was, understandably, focused on survival at the beginning of the pandemic; a plan for the return to 2019 demand was not high on the priority list. Flights were consistently cancelled, baggage was lost, understaffed airline crews were stretched to the limit, and jet suppliers couldn’t produce new jets fast enough.

Increased demand did mean a better pricing environment, but operational hiccups and high oil prices meant not much in the way of profits (or customer goodwill…). 2023 is being set up as a new normal; Delta announced at their June investor day that they’re sunsetting their 2019 comparisons and believe the industry is set up for growth.

The Opportunity

This thesis is based around a few key points:

Airline growth will return and continue its historical trend of following GDP.

The current constraints on the industry will keep a lid on capacity growth and favor large-scale carriers.

Valuation.

Airline GDP

Despite the volatile history of airline profits, air travel revenues have a pretty steady relationship with GDP, averaging ~1.3% over the last 40 years. The make-up of these revenues has changed though; air miles travelled has grown from 55bln miles in 2000, to 90bln in 2019 (~3% CAGR), but airline revenue per mile have decreased, in real terms, from ~¢30 in 1980 to ~¢20 cents today. This reversed in the 2010s, with revenue per mile stabilizing and even beginning to grow. 2022 has seen a pickup in demand to closer to historic levels, but spending is still below the historical average (~1.2% in 2022).

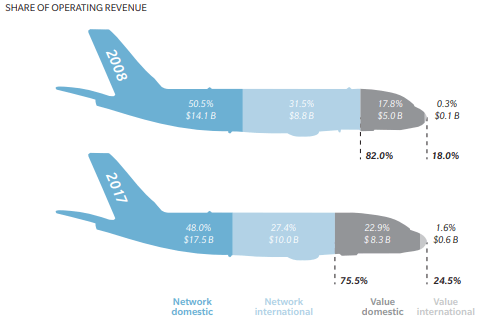

There’s potential for continued growth in revenue per mile as the pandemic created an increase in demand for premium cabin. Delta is probably been the biggest beneficiary of this as their customer base tends to skew wealthier. Their premium cabin revenues have increased from ~$10bln in 2014 to ~$19bln in 2023 (est.), with the mix increasing from 24-32% of total revenue. There is a risk that this was a pandemic phenomenon, as fliers wanted additional distancing space, as well as having more frequent flier miles to use (after a period without travelling); but with business class coming back (even if not ever fully recovering) and boomers approaching retirement, I think the shift in premium mix has staying power (boomers are the wealthiest generation we’ve ever seen). Delta agrees, with their new A321neos, replacement for 757-200, having 5 less seats (194), but 13 more in premium cabin.

Moving forward, I think it’s reasonable to assume the industry gets back to revenue growth in line with historical GDP, and the growth is a healthy mix between miles flown and revenue per mile.

Current Constraints

Solid revenue growth doesn’t mean airlines will produce profits, as more revenue has historically meant more capacity coming online, pushing prices down. Capacity is the most important factor when it comes to determining airline profits. If there’s too much capacity, prices fall quickly as consumers look around for the best price and airlines fight to fill up their flights (a cheap ticket sold is better than an empty seat flown). Consolidation has helped control this as the big four, with >70% of capacity, have significant control over ASM growth. There’s potential for more consolidation, with Jet Blue in the process of merging with Spirit (if approved).

The recovery from the pandemic has constrained capacity for the larger airlines, mainly due to a lack of pilots (there are other constraints like jets, supply chain, FAA staffing etc. but I’m going to focus on pilots). A lot of pilots were offered early retirement in the summer of 2020 as airlines desperately tried to reduce costs. But as demand came back, airlines found there weren’t enough pilots to fly the planes. Airlines have had to cutoff service to smaller airports as they focused on their largest profit centers, and >500 regional jets (planes with <100 seats) are grounded due to pilots (this has impacted service from smaller airports into hubs). All airlines are having this problem, but the problem is expected to take years to resolve, and larger carriers are hiring away from smaller airlines with more attractive pay packages and career opportunities.

There also seems to be a generational shift in the appeal of being a pilot. Only 8% of pilots are <30 years old, and 50% of pilots will reach retirement in the next 15 years. Increasing the retirement age is not simple (although US House recently approved a bill to increase the retirement age to 67), with senior pilots more often flying international routes, where other countries’ retirement ages must be respected (usually 65). Training pilots is, understandably, not quick, taking multiple years and 1500 hours of flight time. The FAA rejected a recent request to lower the 1500 hours rule, but pressure is building to lower the requirement. Smaller airlines appear significantly more invested in lowering the requirement, with larger carriers like Delta actually advocating to leave it in place:

“I don't think this is something that you go to when you start to lower the bar. I think you just have to continue to work through it. So no, I'm not an advocate for that.”

Difficult to not be cynical here, but I’d guess Delta isn’t as worried about the pilot shortage as they’ll come out in better position relative to the smaller players… It will be interesting to see how it develops.

The shortage has increased pilot salaries significantly as the market continues to adapt (Delta agreed to a 34% increase in a four-year deal signed this year), but the impacts will be felt significantly more by Ultra-Low-Cost-Carriers (ULCC) and smaller airlines; their cost structures will struggle, relative to big airlines, to absorb the increases in pilot pay; Spirit’s median pilot pay is ~$125k, compared to Delta at ~$175k (per Glassdoor).

So, a pilot shortage will increase costs for all, including the big four, but the shortage will keep capacity constrained. It should also keep away new entrants; difficult to start an airline without any pilots (end of ZIRP will also help).

Other Tailwinds

The points above are the key factors that I think make the airlines a good bet to produce solid operating results over the next few years (barring macro events). But there’s some other signals that I think hint at a positive future for airlines:

Demand for airlines has become less peaky. WFH has meant passengers are able to travel at quieter times for better prices. This allows airlines to utilize planes more efficiently, increasing ROIC.

New planes are ~20-25% more fuel efficient, helping reduce fuel costs.

Airport investment – Large airlines continue to invest in airports, with some taking advantage of the pandemic to accelerate work schedules, securing gates and capacity at key hubs.

Recency bias – it’s human nature to remember the most recent events. Pandemic is top of mind on macro factors when investors look at airlines; there’s a good chance macro is being overly priced in right now.

The Spirit merger mess with Frontier and Jet Blue shows smaller players will do anything to get bigger (or stop rivals). Jet Blue and Spirit have very different business models, but Jet Blue were willing to do pretty much anything to stop Frontier merging with them (overpay and take on regulators).

Common knowledge at this point but airline rewards continue to grow as banks continue to value the rewards and customers continue to covet airmiles (would like to do a post diving deeper on this at some point).

Risks

The biggest risk to overall airlines profits is a large-scale macro event that kills demand. A pandemic might be the worst kind; reduces demand to 0 and leaves airlines with billions of dollars in assets sitting idle and an uncertain timeframe for a return. It’s almost impossible to predict the timing of these types of events and should be accounted for in position sizing and margin of safety.

A recession is another macro risk that will dent demand, create excess capacity, and lead to worse profit margins. Here, I think the current capacity constraints provide some cover. We still haven’t got back to pre-pandemic capacity overall (2022 capacity was ~85% of 2022), and I don’t believe overall demand for air travel has structurally changed since the pandemic; people still want to travel, and aircraft is still the most efficient way to travel long distances. Air fares would come down, but fuel costs likely provide some relief as oil demand weakens (fuel cost were ~60% higher per ASM in 2022 vs 2019).

International travel has been slower to recover from the pandemic, and a global recession would put another dent in demand. A strong dollar makes the U.S. a more expensive vacation for foreigners but decreases costs for U.S. residents. Subsidies for international airlines are a potential issue (some Middle Eastern countries are happy to subsidize airlines), but people like to travel and I see international demand returning to pre-pandemic levels eventually.

Business travel (usually in premium seats) is ~80% of 2019 and it’s unclear if we ever get back to pre-pandemic levels. The world has proven a lot can be done virtually, but I do think we edge back towards previous levels, even if it doesn’t get all the way back. If you’re trying to sell something, an in-person meeting is still table stakes. I also think boomers, as mentioned above, continue to step in and fill the premium cabin seats vacated by business travel. If you have the money and are 60+, more space and comfort feels like a no-brainer.

Where I could be wrong is the costs and constraints dynamic. Labor costs are rising, but the thesis says this impacts smaller airlines significantly more than large carriers, as well as deterring new entrants. This gives large carriers control over capacity, who have shown over the last decade they can manage capacity to generate a profit (large carriers gave up share in the 2010s as smaller carriers expanded). If for some reason this isn’t the case, I’m wrong…

Valuation

Airlines have had a great 2023, with American, Delta, and United up >40% YTD (Southwest is up ~15% due to their December operational issues), but they all trade still ~5-6x NTM EV/Ebitda. This is still with elevated fuel costs, working with a less efficient employee base (a lot are new hires due to pandemic cuts), and less scale from lower ASM capacity. Using Delta as an example for free cash flow (others are under or overspending on capex), they trade at ~10% NTM free cash flow yield (~$3bln), with ~$6bln of capex, and D&A of ~$2.1bln. I’m not saying we should add $4bln to get normalized free cash flow (Delta plans to spend $6bln for the next few years), but over the last 10 years Delta capex has averaged ~$3.5bln capex vs $2.1bln in D&A; I think this normalized yield is closer to ~15%. Capital allocation strategy is known, with airlines focusing on paying down debt to pre-pandemic levels over the next few years.

Final word

The risk of looking stupid here is very high, if a recession hits or macro event occurs it’s the kind of bet an outsider says, “why were you even invested in an airline”? I think this is how pre-pandemic airline investors were looked at (I’m probably guilty of this), but after looking deeper I think they were onto something. Position sizing is important here given the risk of unknowable events destroying the thesis, but I like the odds. Full disclosure I haven’t invested in an airline yet, but I’m looking closely at Delta.

I'm not sure i'd call it a reversal on the thesis; it was a low probability event that completely changed the outlook for airlines. Think he also mentioned that government assistance was unlikely if he was involved in the name, so perhaps not fair to just look at the outcome and say he sold at the wrong time.

what to make of buffett's multiple reversals on airlines?

if he went into railroads with primarily the same consolidation thesis, then did he just get lucky by buying instead of renting? (am discounting all secondary effects justified retrospectively)