H&R Block Deep Dive (HRB)

I originally became interested in H&R Block (HRB) in late 2019 when I was getting into investing. The obvious selling point of Block was that it was cheap on pretty much any earnings metric and operated in a relatively stable industry (gotta file those taxes). Given the current market conditions I figured I’d make myself feel better and look at a pick that’s worked out (so far).

Block’s biggest issue in 2019 was their businesses focused on assisted tax prep, and DIY solutions like Intuit’s (INTU) TurboTax were consistently gaining share. There were a few reasons I thought Block could limit share losses over the long-term:

I thought people would keep using assisted solutions. There’s value in a person walking you through your taxes (especially a trusted brand). Taxes scare people and for ~$250, you can have a tax pro prepare your taxes and put your mind at ease (win-win).

Their change in pricing reset the business, simplified their offering, and while it impacted revenue short-term, allowed Block to return to topline growth in the assisted category.

The industry has “sticky” customers who tend to return year after year. Block estimates that ~75% of their customers return each year.

After I pulled the trigger and bought the stock the pandemic hit, in person meetings were effectively banned, and the tax deadline got extended. This was a perfect storm for Block, and the stock got hit, falling to ~$13. The concerns were legitimate, if people weren’t allowed to go to Block offices (~50% of them were closed), would people move over to DIY solutions and never look back? Turns out most people still like the idea of human assistance on their taxes, even if it’s virtual.

The stock price has ripped ~55% in 2022 (~$37) as results have come in above expectations and the stability of the industry has attracted investors looking for safe havens.

The Current Situation

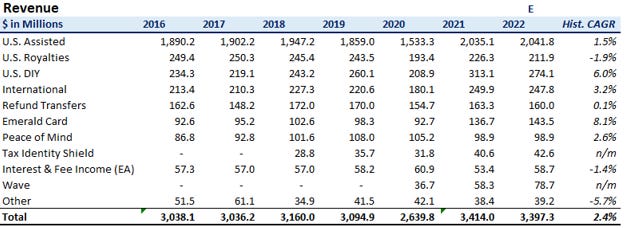

Block’s business is built around tax season, meaning their business centers around 3 months of the year (late January – mid April). The rest of the year the business operates at a loss and analyst calls get a little less interesting, either talking about the upcoming tax season or talking through other growth initiatives that have a small impact on HRB’s overall financial performance. Pretty much all their revenue streams apart from Wave (purchased in 2019) are built off tax services. I’ve summarized HRB’s revenue streams below:

U.S. Assisted - 60% of revenue

Tax return assistance provided in company owned offices (~6.7k offices). The Net Average Charge (NAC) is ~$235 and they prepared ~8.3mm in 2022.

U.S. Royalties – 8% of revenue

Franchise owned H&R Block stores that perform the same services as company owned stores. Block receives ~30% of gross revenue from these offices. There are ~2.7k franchise offices in the U.S., with Block actively buying back franchises (~125-150 a year).

U.S. DIY – 8% of revenue

A lesser-known offering but still widely used (#2 DIY solution behind Intuit’s TurboTax), Block offers a DIY tax service that allows customers to file using their software (~8.2mm filed in 2022). The NAC is ~$35 but has high margins.

International – 7% of revenue

Same assisted services as above but for international clients (Canada, Australia, Other).

Refund Transfers – 5% of revenue

Allows clients to choose how they receive their tax refund (e.g., load to their Emerald Card) and gives them the flexibility to deduct HRB’s tax fees from their refund.

Emerald Card/Emerald Advance – 3% of revenue

The Emerald Card allows customers to receive tax refunds directly from the IRS directly (on a prepaid debit card). The card operates as a normal prepaid debit card and funds can be added throughout the year. Emerald Advance offers credit lines directly through offices, typically from mid-November through mid-January, in an amount not to exceed $1,000. Depending on the circumstance, the L/C may be used year-round.

Peace of Mind – 3% of revenue

Offering where H&R Block will represent clients (U.S. and Canada only) if they are audited by a taxing authority and covers costs in case of an error by H&R Block ($6k cap for U.S. client and $3k CAD for Canadian).

Tax Identity Shield - 1% of revenue

Offers assistance in protecting a client’s tax identity and provides access to services that will restore their identify if required.

Interest & Fee Income – 2%

Interest fees on Emerald Advances.

Wave – 2% of revenue

Purchased for ~$400mm in 2019. Provides small business solutions, focused on 1-9 employees. Uses a freemium model by offering basic accounting software for free, and charging for other services like payment processing, payroll, and invoicing services.

Other - 1% of revenue

No information provided by HRB.

2020 & 2021 fiscal years are a little messy as they don’t include a full tax year (fiscal years shown above are for years ended April 30th apart from 2022). 2020 has a partial year due to the tax deadline being extended until July 15. 2021 included the end of the 2020 tax season in Q1 and then the 2021 tax deadline was extended until May 17, meaning some 2021 tax revenue was moved into 2022. To account for this, management moved their fiscal year-end to June 30 (2-month stub period May 1, 2021 – June 30, 2021), so going forward results will be comparable (2022 estimates are 1 full tax season - doesn’t include extended 2021 tax return numbers).

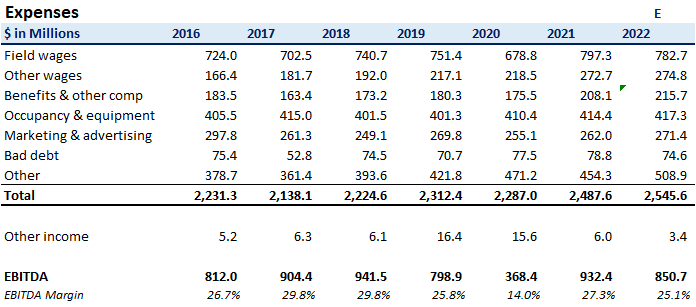

Block generates normalized EBITDA margins of ~25%, with ~60% of EBITDA converted into free cash flow. EBITDA margins have come down slightly over the last few years due to reinvestment in the business (e.g., assisted repricing, Wave, and Spruce which are discussed in more detail later).

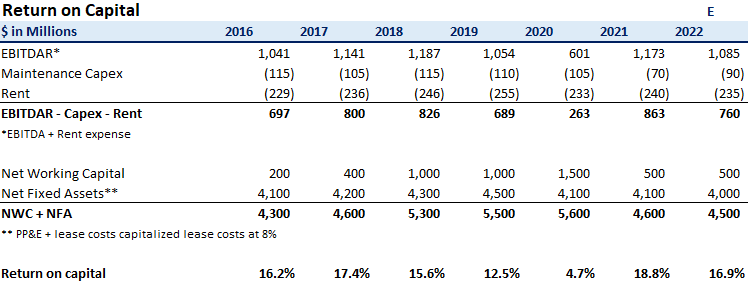

Normalized return on capital is ~16%. I’m using an adjusted version of Greenblatt’s ROC calculation as Block’s offices are leased and have 3-year terms. This means leases are understated on the balance sheet (they need to renew them); I’ve capitalized leases at 8%. It’s also worth mentioning they carry excess cash at the end of the tax season as they operate at a loss for 3 quarters (positive net working capital balance):

Greenblatt’s formula:

(WC + Net Fixed Assets) / (EBIT).

Adjusted:

(WC + Net Fixed Assets) / (EBITDAR – Capex – Rent).

The business trades at a forward EV/EBITDA multiple of ~7.5x. This is slightly higher than it has been historically (~7x) but is still cheap on an absolute basis (~9% free cash flow yield).

How Does HRB Work from Here?

Now to the important question, how does Block work from here at its current valuation. I think there’s 3 key issues to get comfortable with before investing in Block now:

What happens to assisted tax prep market and can Block hold share?

Is management going to allocate capital efficiently?

Is the valuation still reasonable?

Assisted Market

This one is obvious. Assisted is Block’s core business (assisted offering are ~75% of revenue) and the stock will eventually follow Block’s performance in the category. Software-based solutions (DIY) will continue to take share and with a slow growing market, getting comfortable with how the changing industry impacts Block is important.

The IRS gives provides information on the overall market on their website, detailing the following:

Number of filers (including e-filer)

Preparation method (self-prep or prepared by professional)

Refund information (avg. refund etc.)

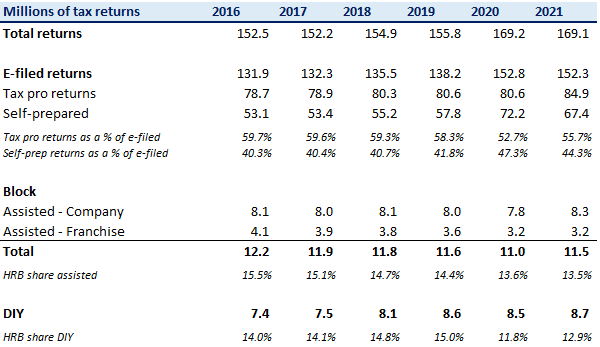

The pandemic has made it hard to anchor off 2020 and 2021, this time due to stimulus payments. The IRS has estimated there were ~8mm additional filers, who filed a tax return with $0 income, specifically to get pandemic aid (Block estimates more). I’m using tax-pro returns as a proxy for the assisted market, with self-prep a proxy for DIY.

Pre-pandemic we were seeing just under 1% growth in the # of returns filed, with assisted losing ~60bps of share a year to DIY. This means assisted volumes are staying roughly flat despite losing share to DIY (~80mm).

Block’s share of the assisted market had been steadily decreasing but the pricing reset helped stabilize share and management stated they gained share in assisted in 2021 (first time in a decade - numbers I’m using show a 10bps point loss).

It’s hard to know what can be taken from the 2020 and 2021 tax seasons, but Block’s performance was way above expectations given their model is based around in-person meetings. The move to highlight virtual assisted options (e.g., digital drop off), along with more transparent pricing has increased value to customers and I think can help them hold share moving forward.

The biggest risk to Block holding share is Intuit’s move into the assisted space (in 2021). It will be interesting to see how their assisted offering develops but my guess is converting a DIY TurboTax customer to an assisted offering will be a lot easier than pulling in outside customers (a lot of marketing spend to change the public perception of TurboTax; everyone sees TurboTax as a DIY option).

I think assuming ~80-82mmmm assisted returns with Block holding share ~14% is a reasonable assumption. Block should be able to turn this into low single digit revenue growth with price increases.

Management

One of the criticisms of Block has been management; Block generates a significant amount of free cash flow (~$500mm a year). The problem is there’s not many opportunities to reinvest in the tax business that offer the same returns on capital. In this scenario management becomes extremely important as what they choose to do with the cash determines whether that $ of free cash flow is worth a $ to us as investors.

Previous management had tried other industries; they operated a bank from 2006-2015, before selling to Bofl (now Axios). Current management, brought in 2017 after previous management was fired, performed a strategic review on the business made the following moves.

Reset pricing (2019)

Mr. Jones believed pricing had become too complicated and reset pricing to make the cost of service transparent to customers. This meant a temporary hit to revenue but has allowed the business to stabilize their share in the assisted category.

Wave (2019)

The purchase of Wave (~$400mm purchase at ~9x revenue), while not a disaster, was too expense, even though the business added strategic value. Wave offers free accounting services to very small businesses and then monetizes customers by charging for add on services such as payment processing and payroll services. Management thought they were getting access to a fast-growing small business customer base and could funnel Wave clients to Block for tax prep services (small businesses have a higher NAC than retail customers). This has proved true with management disclosing mid-single digit growth in small business tax prep volumes (Q3 2022 earnings call). The issue is they simply overpaid, and investors are wary of Block trying to buy their way out of their inherent seasonality.

Block Horizons (2021)

This was Mr. Jones’ new strategy to focus on Block’s competitive advantages. The strategy centers around 3 pillars:

Small Business – Increase offerings to small businesses by using Wave and Block (currently ~2.4mm customers), to increase monetization by funneling Wave clients to Block’s tax offerings and increasing the services Block offers to their own small business clients. Block estimates that a 1% increase in small business tax share leads to ~$60mm in revenue. Also, Block has trained employees to offer small business services such as quarterly tax planning. Given the Wave acquisition has already happened (sunk cost), the strategy makes sense and doesn’t cost much to pursue.

Financial Products – Focuses on the underbanked with the Emerald Card/Emerald Advances and the new Spruce app. Block has access to ~8mm underbanked customers, and management believes the Spruce mobile banking app can offer value add services. Block didn’t obtain a bank charter to launch Spruce and has no plans to (stated at their Spruce deep dive by CFO Tony Bowen). They’ve partnered with MetaBank for these services and believe they have favorable economics. Capital committed to launch Spruce is relatively low (“$10s of millions” per Mr. Bowen) and, while the platform doesn’t offer anything a normal bank can’t, they do have unique access to low-moderate income customers. Block will monetize these users through either ATM fees (outside of the 55k partner ATMs) or through spending activity on the card (card offers no interest to customers). While still early days the platform looks to have gained some traction and management has committed to reporting useful metrics such as the # of sign ups and dollars deposits (150k sign ups and ~$60mm in customer deposits as of April 30th, 2022).

Block Experience – The goal of Block Experience is to improve the core tax prep offering and to increase the use of Block’s digital capabilities in assisted categories. Management wants to offer customers more choice in how they file their taxes with Block (drop of, submit online, traditional retail office appointment etc.). Analysts have asked if this new push could potentially reduce Block’s retail footprint and increase margins. Management believes it can reduce the square footage they need, but the digital shift doesn’t remove the need for stores as they want to cater to customers (same number of stores but less square feet per store). They also plan to increase monetization in DIY by offering certain add-ons like tax-pro review (have a CPA review your self-prepared return).

The pandemic has showed the value of these services and is an area where Block can differentiate themselves from independent preparers. This will also help offset any pressure from TurboTax and their new assisted service.

Buybacks

Block has bought back a lot of stock over the last 5 years, spending ~$3.5bln since 2016 to retire ~30% of their stock. The $2bln 2016 buyback wasn’t, in hindsight, at great prices (~$35 a share), but since Mr. Jones took over in 2018, they’ve been more opportunistic, continuing to buyback shares in 2021 when the stock was depressed and uncertainty was at its highest.

I like the buybacks (even if the prices aren’t as attractive now) mixed with a consistent dividend; while it might not be theoretically optimal, it gives consistent capital back to shareholders and allows management some flexibility to concentrate the share count when they believe the shares are cheap. The other options are things like acquisitions which I would strongly prefer management to avoid. They’ve hinted they don’t plan to make any acquisitions, so I think we can feel reasonably good about management’s capital allocation strategy moving forward: consistent dividends, buybacks (hopefully opportunistic), and a small amount of internal investment in the business.

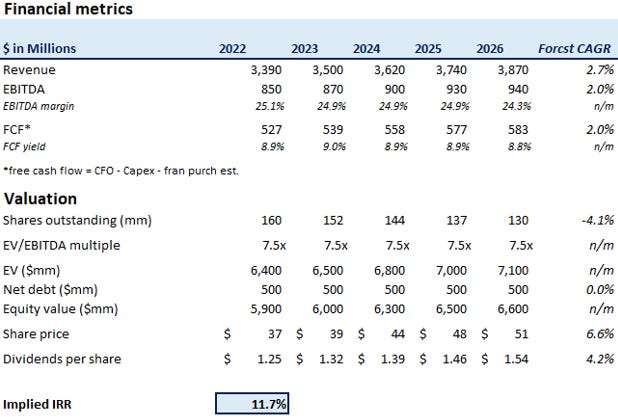

Valuation

How does the above translate into a valuation? Given the messy last few years and the change in fiscal year I’m going to use management’s guidance for 2022, which I believe is accurate (9 months into the year) and then project out to 2026. I’m not going to go over all the revenue streams but will focus on what I believe are the key drivers.

U.S. Assisted

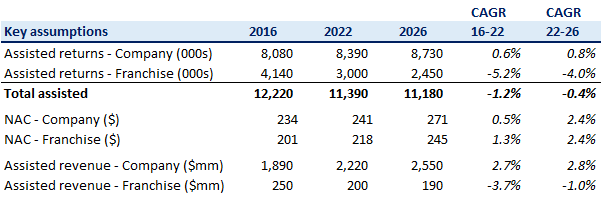

For the full 2022 tax season Block filed ~11.3mm assisted returns (company and franchise) and, like I discussed above, I think they can hold share steady over the next 5 years (~14%) with overall market staying flat (growth of overall market offsets share losses to DIY). This means 0 growth in assisted returns over the forecast period. Block is buying back franchises (~125-150 a year) which will increase revenue ~1% a year (franchises pay a royalty of ~30% of sales and Block picks up that remaining 70% when they buy the franchises out). This reduces margins which I’ll account for in the EBITDA margin.

DIY

Block filed ~8.2mm DIY returns in the 2022 tax season. Block lost share in the DIY market throughout the 2022 tax season. They claim there were some execution issues and saw some improvement in the second half of tax season with some different messaging, but it’s hard to see how Block can hold share and slow TurboTax’s gains. I’m predicting a 12% share of a growing DIY market in 2026 (down from ~14% in 2019) and expect Block to push through modest price increases. The big selling point for Block is they price below TurboTax and have a good all-round product, so even though I’m predicting share losses, they’ll grow revenue at a ~4% CAGR.

This gives revenue of ~3.85bln in 2026, mainly built of the assumption that Block holds share in assisted, loses a little share in DIY, and Wave grows ~16% CAGR. This assumes no real success from Spruce, and the rest of the revenue streams I’ve kept flat (doesn’t have a large impact on stock performance).

EBITDA

EBITDA has margins have decreased over the last 5 years, mainly due to the Wave acquisition (loss making business), franchise buybacks (increase revenue but decrease EBITDA margins), and some overall wage inflation (non-tax prep related). I see margins continuing to slowly decline due to the trends outlined above but Block’s main expense, tax prep wages, is based on a preparers book of business (~30% commissions). This will help keep margins stable (tax prep wages make up ~30% of operating expenses). I’m predicting ~24% margins in 2026, leading to ~$950mm of EBITDA.

Summary

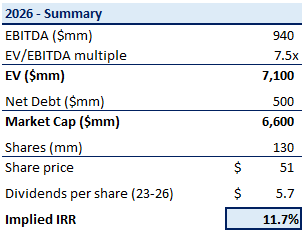

Using a 7.5x multiple (EV/EBITDA) and a share count reduction of ~30mm shares (~$350mm buybacks a year), this gets us a $51 share price in 2026 with ~$5 a share in dividends, an implied IRR of ~12%. I think a flat multiple is appropriate; if the business holds assisted share over the next 5 years it will have proved its long-term viability and a ~9% free cash flow yield isn’t a stretched valuation.

I still think there’s value in Block but I’m not going to add to my position currently. I’m not selling as I understand the business and I don’t like to sell unless the valuation has become extremely stretched (I don’t think that’s the case here).

The valuation does, however, now require solid performance from Block for an adequate return, rather than a stabilization of the assisted category leading to large gains (which it did with the stock ~$25 at the start of the year). Thanks for reading.

Appendix A