AT&T ($T) – One Pager

AT&T ($T) – One Pager

I recently purchased some AT&T shares. Low single digit Ebitda growth coupled with a 6% dividend yield and debt paydown to 2.5x EV/Ebtitda create an interesting opportunity.

I think the current set up for AT&T (T 0.00%↑ ) is interesting; the spin-off of WarnerMedia and the partial sale of DirecTV has allowed management to refocus the business, formulate a coherent capital allocation strategy, and cash flow should accelerate as 5G investments slow. The business currently trades for ~7x NTM EV/Ebitda (for reference VZ 0.00%↑ is ~7x and TMUS 0.00%↑ ~9.5x).

Refocused business

Mr. Stankey, despite being involved in the media/video deals as COO, has simplified the business since becoming CEO in late 2019. First, in 2021, DirecTV was taken off the balance sheet in a ~$17bln deal with TPG. AT&T still own ~70% (I’ll get to that in the valuation), but they do not have operational control. They also spun-off WM in April 2022 and finalized the destruction of ~$50bln of shareholder value.

The new look business is focused on two main products: mobility and fiber. Mobility makes up ~2/3rds of the revenue and slightly more of the Ebitda base. Mobility is growing in 3-5% range as they’ve begun to take back some share. Their simplified pricing structure and promotions have revived their mobile offering and they’ve added ~6mm postpaid phone subs over the past 2 years. Industry adds are starting to moderate, but management believes there’s room for some ARPU growth to help offset slowing adds. I also think there’s a long-term tailwind from 2 phone customers (personal and business), as businesses focus on security and the office phone continues its slow death; only ~6% of smartphone customers had two phones as of May 2021.

Their consumer wireline business has also reached an inflection point, with fiber subs now more than legacy copper; this is starting to drive topline growth. They plan on expanding fiber to ~30mm passings (~24mm currently) by the end of 2025 and will continue to rationalize their copper footprint. This will mean expanding margins as they spend less on low penetration copper and higher margin fiber continues to take over the segment.

Note: I still believe in the overall cable thesis I’ve laid out in previous posts, but I think with AT&T’s current valuation, 40% penetration in fiber is more than enough to generate a reasonable return here. I also think AT&T has advantages over smaller fiber providers due to their scale, internal financing, and convergence optionality. Quote from AT&T CFO at recent conference:

“we have a pretty meaningful uptick in our wireless penetration when we have fiber ”.

The largest headwind has been the business wireline segment (~20% of revenues and Ebitda) and management expects this to continue in 2023. They have reduced the products they offer and believe Ebitda will stabilize over the next year as their fiber buildout creates opportunities, and they continue to focus on higher margin products. It’s hard to have much confidence here, but even with mid-to-high single digit declines, 2-3% overall Ebitda growth is achievable.

Capital allocation

We have a great line of sight into what AT&T is going to do with their free cash flow over the next few years. They’ve committed to ~$8bln in dividends (~6% yield) and plan to reduce net debt to ~2.5x Ebitda by the beg. of 2025 (originally aiming for end of 2023). Current debt is ~$130bln, with a goal of ~$110bln (assuming ~$44bln in 2025 Ebitda). I like this setup; we know where the cash is going and it all benefits shareholders.

Cash flow/valuation

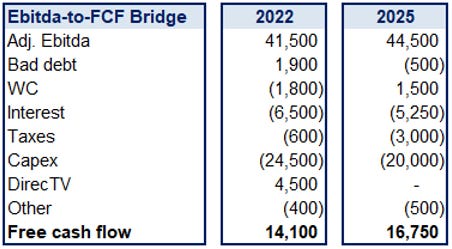

This is where it gets interesting. 2022 Ebitda was ~$41.5bln, with cash flow of ~$14bln; assuming 2-3% Ebitda CAGR through 2025, and making some adjustments based on management’s comments, I think ~$17bln of free cash flow in 2025 is very possible.

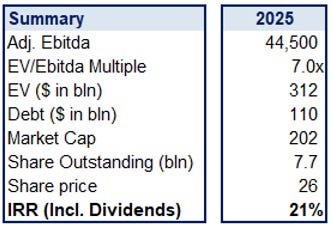

Working capital position will improve as wireless adds slow; this is due to upfront acquisition costs being amortized (cash spend is at the beginning of the relationship but GAAP requires costs to be amortized over expected life); management expects this to happen in 2023. Interest expense drops ~$1.5bln as they reduce their debt balance (I’m using ~4.5% interest rate, up from ~4% now – ~95% of their debt is fixed with avg. maturity >15 years). I’ve adjusted cash taxes up to ~$3bln ($30bln pre-tax * 21% tax rate, with half deferred - some guess work here). Capex spend is down to ~$20bln as 5G costs roll off; there’s also ~$2.5bln of growth capex here from the fiber build out ($1k cost per passing and $500 cost to connect). Assuming there’s no more juice in DirecTV by 2025 (no value assigned to DirecTV), we get ~$17bln of free cash flow, on a current market cap of ~$130bln. Another way to look at it, keeping 7x as the multiple we get a share price of ~$26 in 2025 with ~15-20% of the market cap returned through dividends, an IRR of ~20%.

I recently purchased some shares.

I've enjoyed reading all your posts.

Do you know why AT&T's broadband segment only has 30% EBITDA margins? Now that they no longer consolidate DIRECTV/a much lower margin video business, I would have thought the margins here would be very high. This would seem to have implications for FYBR and other fiber overbuilders who I believe are underwriting much higher margins on these investments.